Financial Planning

The strategy referred to as ‘spouse contribution splitting’ is typically implemented in July and allows couples to potentially increase the amount they can hold in the tax-free pension phase in retirement. A couple’s ability to access superannuation and their eligibility for certain entitlements may also be improved as a result of implementing this strategy each year.

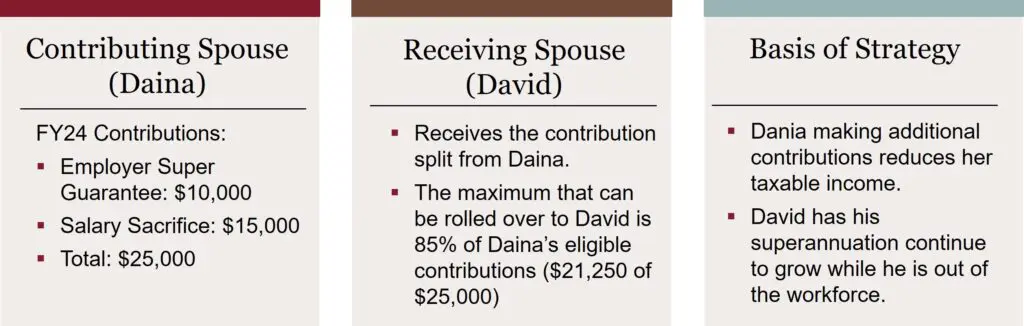

Spouse contribution splitting is a process where one spouse (the contributing spouse) transfers up to 85% of their superannuation contributions made in the previous financial year to their partner (the receiving spouse). The maximum is 85% because 15% is taken out for contributions tax. Contributions that can be split include employer contributions, salary sacrifice arrangements and personal contributions, but excludes any contributions that have already been taxed, such as after-tax contributions. These contributions must be within regular contribution limits (discussed here).

To illustrate how a couple may use contribution splitting, take the example of Daina and David. Daina is currently working fulltime as a consultant while David is caring for their young family. Through the year, Daina’s employer contributes to superannuation, and she adds to this through a salary sacrifice arrangement. Daina and David engage in a spouse contribution strategy as outlined below.

To be eligible to utilise spouse contribution splitting, the receiving spouse must be under the age of 65 and not retired. Other considerations include:

Spouse contribution splitting is a valuable strategy for couples looking to optimise their combined retirement savings and tax positions. An Evans and Partners financial adviser can help assess your financial situation and outline how your family can benefit from a spouse contribution splitting strategy.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product. Past performance is not a reliable indicator of future performance.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.