Financial Planning

Learn more about Division 296 and how it may affect you here.

In October 2025, the Australian Government announced significant changes to its proposed Better Targeted Superannuation Concessions (BTSC) policy, better known as the Division 296 Tax. We now have draft legislation to support the proposed changes. The legislation provides crucial detail on implementation mechanisms whilst leaving several technical elements subject to pending regulations. This increases the importance of staying informed on what is one of the most significant changes in superannuation policy in over a decade.

After three years of announcements and amendments, the latest iteration of the Division 296 Tax was tabled in February 2026 as the Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026. Alongside the name change, the new Bill formalises the amendments that were first announced in October 2025 and discussed here.

In its current form, Division 296 is a two-tiered additional tax:

The above taxes will apply to all income and realised gains attributable to the portion of the balance above the three-and-ten-million-dollar thresholds. These will also be subject to indexation in increments of $150,000 and $500,000 respectively. The start date for the proposed tax is 1 July 2026.

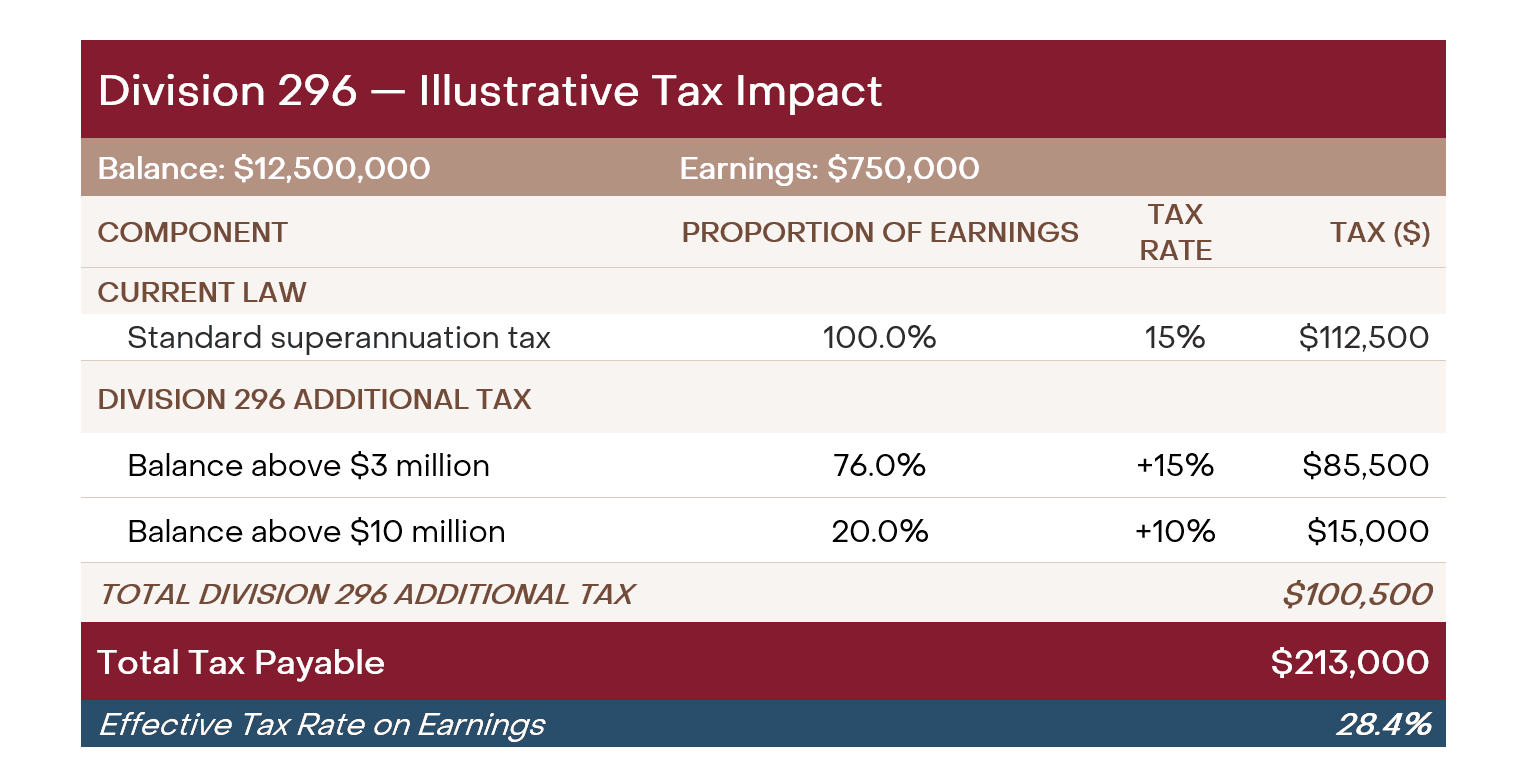

Consider Charlotte, who holds $12.5 million in superannuation accumulation phase and earns $750,000 on this in the 2026–27 financial year. With her balance exceeding both Division 296 thresholds, she will be subject to additional tax.

The standard 15% superannuation tax (assuming no CGT discounts are utilised) produces an initial liability of $112,500. Division 296 then applies proportionally, with an additional 15% on 76% of her earnings (the share above $3 million) and a further 10% on 20% of her earnings (the share above $10 million), adding $100,500 in additional tax.

Charlotte’s total tax bill reaches $213,000, payable from either her superannuation fund or personal cash reserves. Notably, her effective tax rate of 28.4% remains well below her marginal income tax rate of 47%, inclusive of the Medicare levy.

Source: E&P

Please note, the table above is for illustrative purposes only and does not constitute advice. Calculations are based on proposed legislation and are subject to change.

Much of what remains uncertain with respect to Division 296 is its implementation. To that end, the draft legislation released in February 2026 provided detail on three key aspects:

An individual’s exposure to Division 296 Tax will be dependent on the higher of their starting or ending Total Superannuation Balance (TSB) each financial year. This means withdrawals made throughout the year will not help avoid the tax.

The Government has, however, announced a transitional rule for 2026–27 in which only the super balance on 30 June 2027 will apply.

Strategic implication: In the period leading up to 30 June 2027, individuals who reduce their balance below $3 million by 30 June 2027 would be exempt from Division 296 Tax in the 2026–27 financial year. This strategy is highly individual, and the right decision depends on a range of personal financial factors..

Self-managed Superannuation Funds (SMSFs) can reset cost bases for assets to the value as of 30 June 2026. This reset applies for Division 296 purposes only and does not change the cost base used for income tax purposes (i.e., the value used when calculating capital gains when selling an asset).

This decision must be applied across all or no SMSF assets and is irrevocable. For individuals wanting to make such an election, it must be done by the 2026–27 tax return lodgement date.

Strategic implication: Individuals may elect to reset cost bases where an SMSF holds significant unrealised gains. This action may help to reduce additional tax from Division 296 when the assets are sold.

SMSFs subject to Division 296 require an annual actuarial certificate to verify fair and reasonable earnings allocation between members. This represents an additional annual compliance cost for affected funds.

Strategic implication: Individuals must ensure their SMSF has sufficient liquidity to meet such costs and to pay their Division 296 Tax liability should they wish to do so from the superannuation environment, noting this can be paid personally as well.

The Government is yet to finalise a number of matters with regard to Division 296. For SMSF investors, this includes details on the certification methodology for actuarial certificates. There is also a pressing need for detailed rules for calculating realised earnings and attributing these correctly to individuals.

The most significant area of uncertainty lies with Defined Benefit Pensions. It is expected a family law approach will be used to create a notional capital amount that forms a permanent TSB value that cannot be withdrawn or reduced. This restriction will also apply to pre-retirement members, who will only be able to manage Division 296 exposure through strategies involving their accumulation component, as their defined benefit component remains locked until retirement.

Division 296 remains one of the most significant superannuation policy reforms in recent years. Given the confirmed 1 July 2026 commencement date and pending regulations, our recommendations are:

As legislation continues to evolve, it is recommended individuals seek financial advice as early as possible. An Evans & Partners financial adviser can help you manage Division 296’s impact and provide guidance on strategies that can be implemented to mitigate future liability.

Learn more about Division 296 and how it may affect you here.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

The information contains projections and forecasts (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group and its related entities make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information. Results are only estimates, the actual amounts may be higher or lower. We cannot predict things that will affect your decision, such as changing interest rates. Seeking professional personal advice is highly recommended before acting on any such assumptions. Past performance is not a reliable indicator of future performance.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.