Financial Planning

The start of a new year provides an opportunity for meaningful financial conversations across generations. At first, the conversation may focus on the ‘sacrifices’ we should make. We all have a subscription we rarely use, a bill we have never compared, or a guilty pleasure we indulge in more often than we should. Families who engage in these conversations regularly can transition to more impactful discussions. For most people beginning their investment journey, the hardest part of investing is simply deciding when to start. Markets are constantly shifting, economic headlines can feel unsettling, and uncertainty often leads to waiting for the perfect moment. Support from family can help navigate these challenges and build confidence, particularly as long-term investment success is seldom about timing. It is about staying invested and harnessing the power of compounding.

Saving is important, but on its own it is unlikely to achieve the long-term financial goals many aspire to. Investing is where growth occurs. Three elements are essential for a successful long-term investment plan:

Intergenerational advantage: These foundational elements are strengthened through intergenerational financial planning. Engaging with experienced family members and established advisory relationships provides valuable perspective on long-term wealth creation strategies and can help younger investors navigate complex financial decisions with greater confidence.

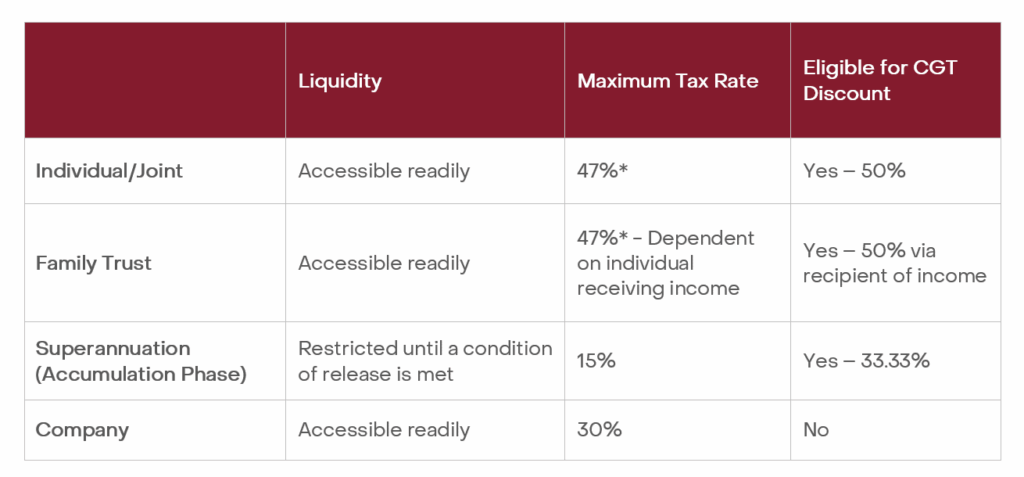

The most complex component of an investing foundation is understanding the structures available to hold your investments. While many factors determine which structure is most appropriate, some of the more common options and their characteristics include:

*Including the Medicare Levy of 2%.

Please note, the table above is for illustrative purposes and is not intended as an exhaustive comparison between structures. The table does not constitute advice.

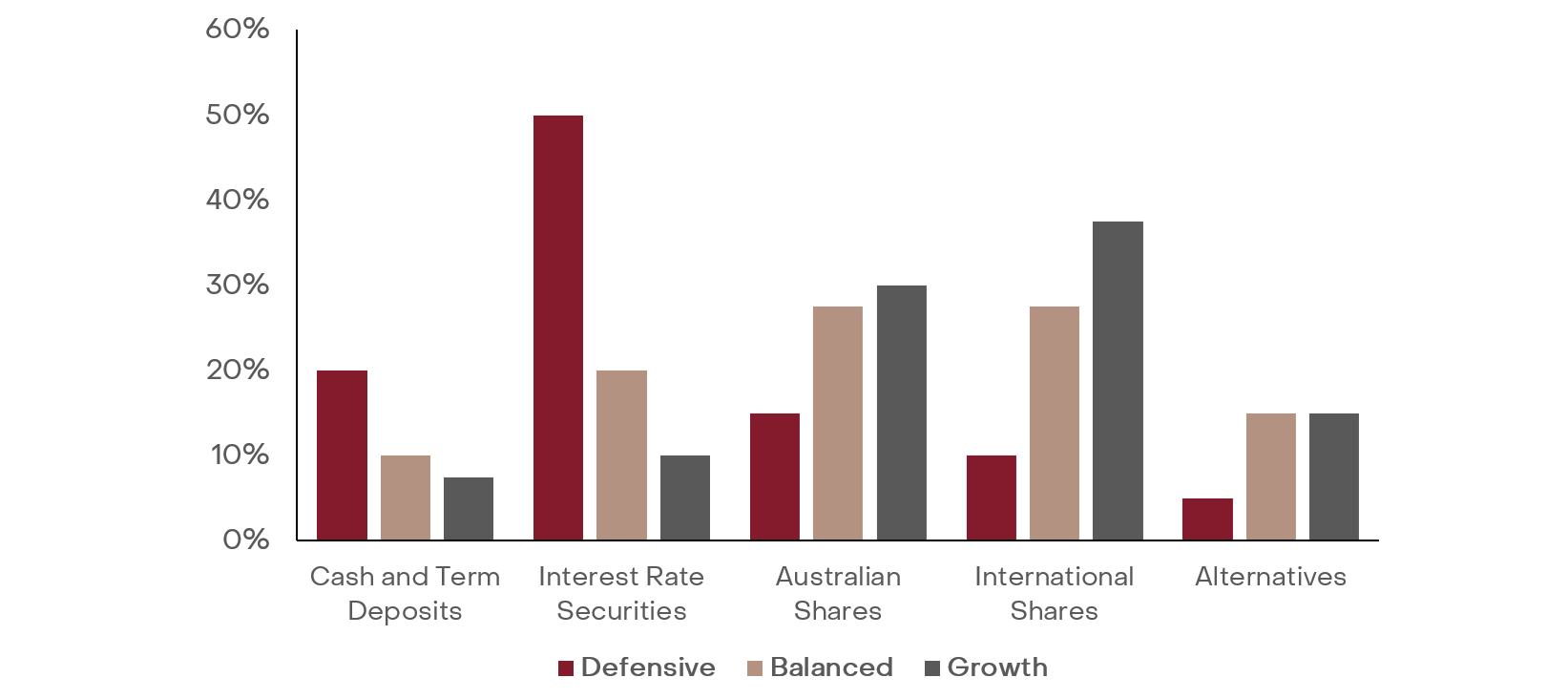

Once you have selected an investment structure, your financial goals and timeline will help determine the type and mix of assets that are appropriate. The example below demonstrates sample portfolios for defensive, balanced, and growth-focused investors. As risk tolerance increases, portfolios generally hold less Cash and Interest Rate Securities in favour of greater allocation to growth assets such as Australian and International Shares. This is where the guidance of a professional adviser becomes essential, helping to curate a portfolio within the correct structure that aligns with your specific goals, risk tolerance, and investment horizon.

Source: E&P

Please note, the graph above is for illustrative purposes only and does not constitute advice.

The final hurdle many investors face is psychological. Many delay investing because they fear markets are too high or that a better opportunity will appear. However, waiting for certainty often results in missed opportunities. Investing consistently reduces the pressure of trying to choose the perfect entry point and helps smooth market volatility over time.

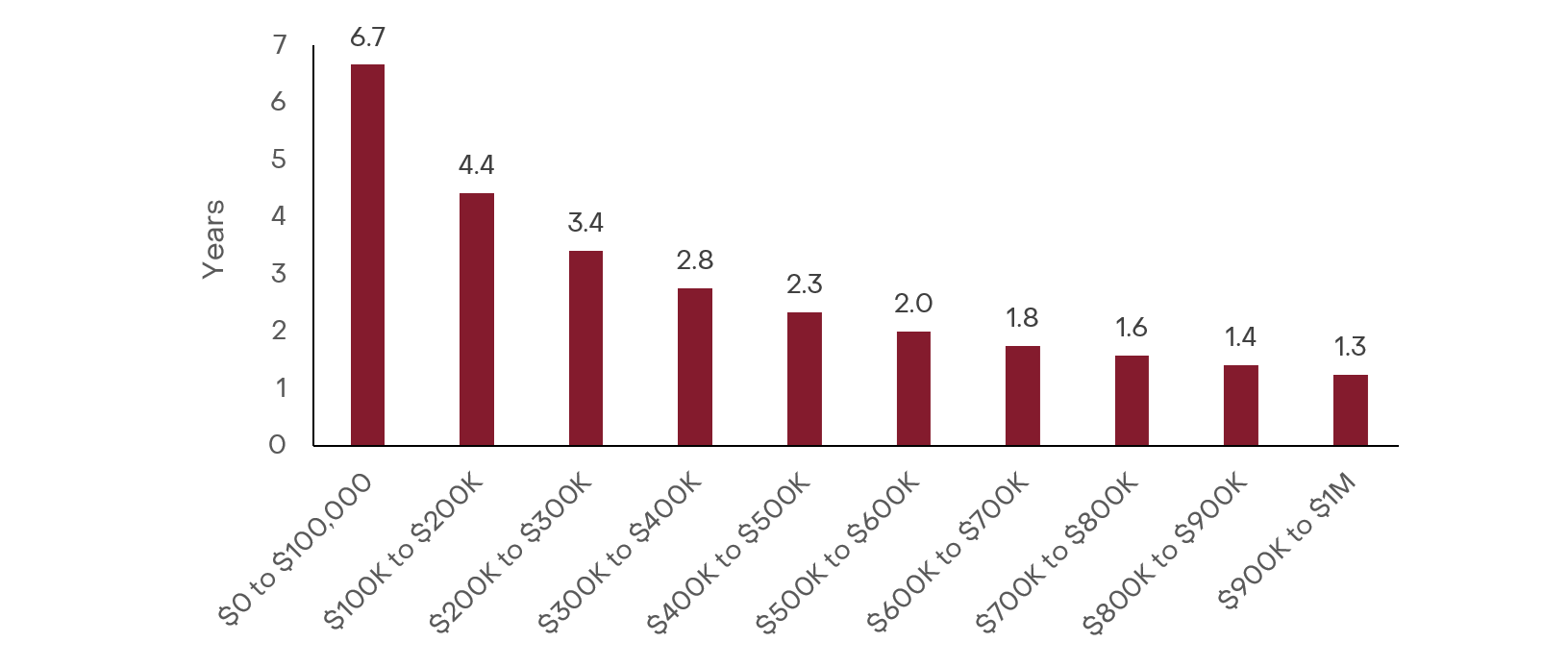

Starting early, whatever your age, gives your wealth more time to compound. Consider Freya, a graduate establishing her career, who under the guidance of her parents and their Adviser commits to contributing $1,000 per month to a diversified portfolio. Her goal is to grow the portfolio to one million dollars. The first $100,000 takes nearly seven years to accumulate, whilst the last $100,000 takes just over one year.

Source: E&P

Please note, the above graph is for illustrative purposes only and does not constitute advice. The actual outcome will vary based on market movements, fees, tax paid, and your relevant personal circumstances. The 7% return used in this example is not applicable to all investment returns. Individual performance may also differ due to timing of entry or investment size of holdings.

Delaying the decision to invest compresses the available timeframe and increases reliance on higher contributions or stronger returns later. In Freya’s case, if she delayed this strategy by a single year, she would need to contribute an extra $80 per month. After three years of inaction, the additional contribution rises to $278 per month, and by the fifth year it reaches $520 per month.

Starting to invest should not be seen as a single decision. It should form part of a broader financial plan, shaped by your budget, cashflow, and timeline. From there, an Evans & Partners financial adviser can provide personalised guidance to curate a portfolio aligned with your goals and risk tolerance.

Investing can feel daunting at first, and progress may be slow initially, but compounding works quietly in the background. Over time, momentum builds, and meaningful wealth can be created.

This article was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

The information contains projections and forecasts (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group and its related entities make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information. Results are only estimates, the actual amounts may be higher or lower. We cannot predict things that will affect your decision, such as changing interest rates. Seeking professional personal advice is highly recommended before acting on any such assumptions. Past performance is not a reliable indicator of future performance.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.