Financial Planning

A significant tax change is now law. From 1 July 2026, individuals with a Total Superannuation Balance (TSB) above $3 million will pay an additional 15 per cent tax on the proportion of their superannuation earnings attributable to balances above that threshold. For those with balances above $10 million, a further 10 per cent applies to earnings on the portion above that level.

Embedded in the legislation is a transitional provision that is relevant to many SMSF members, particularly funds with assets that have appreciated significantly over time. This provision allows members to reset asset cost bases, potentially reducing the future capital gains tax (CGT) liability that would otherwise apply under this regime. But, acting requires understanding both how the mechanism works and its limitations. Importantly, this is a one-time opportunity and time to act is limited, so understanding it now, before the window closes, matters.

The election to reset asset cost bases is available to any complying SMSF with six or fewer members. It does not require any member to be above, or ever reach, the $3 million threshold, only that the fund holds directly owned CGT assets.

Fund holders should consider if their fund is likely to exceed $3 million in the future, as it may be prudent to take advantage of the one-off election and reset cost bases now.

Division 296 taxes the proportion of a member’s superannuation earnings attributable to balances above $3 million at an additional 15 per cent. Capital gains on assets sold within the fund form part of that earnings calculation. For many SMSFs, assets such as property or shares have been held for a decade or more and carry significant unrealised gains. Without the cost base reset, those historical gains will attract Division 296 tax, in addition to regular capital gains tax, when the assets are eventually sold.

The Treasury Laws Amendment (Building a Stronger and Fairer Super System) Act 2026 allows eligible SMSFs to elect to treat the market value of their CGT assets as at 30 June 2026 as the new cost base for Division 296 purposes. Any gain that accrued before that date is effectively quarantined from the Division 296 calculation. Only growth from 1 July 2026 onwards will be included when an asset is eventually sold.

The election is made at the fund level and must cover every CGT asset held directly by the fund on 30 June 2026. It cannot be applied selectively, which means a fund cannot reset assets with large unrealised gains while excluding others. Where a fund holds a mix of appreciated and depreciated assets, the effect of the election on the full portfolio is what matters. Once made, the election cannot be revoked.

The reset covers assets owned directly by the fund. Assets held through other structures, such as unit trusts, are treated differently and should be considered separately.

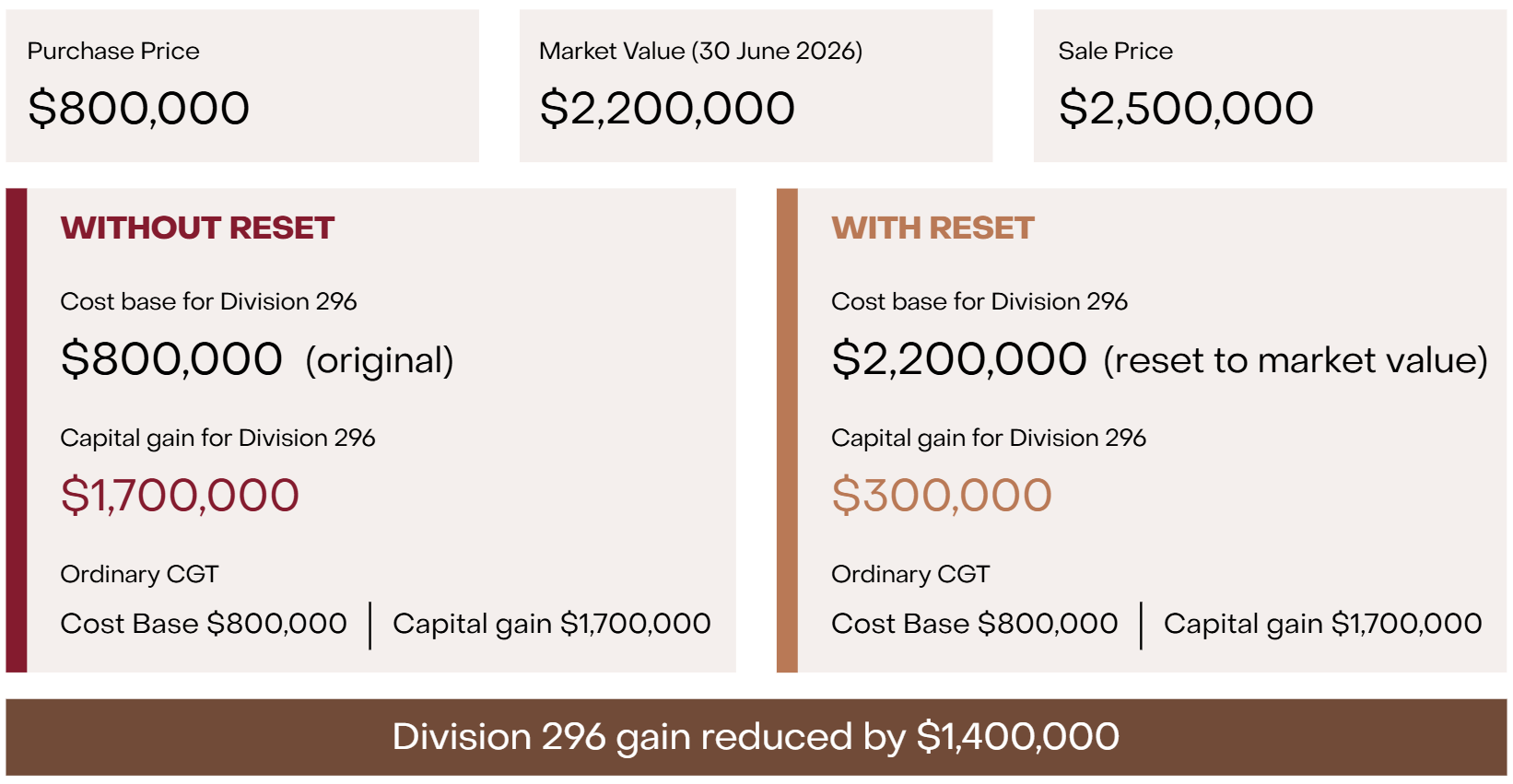

It is important to understand that the reset applies for Division 296 purposes only. When a fund sells an asset, two separate calculations apply: the ordinary CGT calculation (which continues to use the original cost base as it always has) and the Division 296 earnings calculation (which uses the reset cost base from 30 June 2026). The two are independent so resetting the Division 296 cost base has no effect on the fund’s ordinary CGT position.

The example below illustrates how the two calculations sit separately for a single asset.

Source: Evans and Partners

That gain reduction translates to a significant tax saving. Here is how the numbers work for a member with a $5m total superannuation balance and assuming that the asset has been held for at least 12 months.

Source: Evans and Partners

Because the election is all-or-nothing, funds holding assets that have fallen in value since purchase face a specific risk. Resetting a depreciated asset locks in a lower cost base for Division 296 purposes, and any resulting Division 296 loss in the year of sale cannot be carried forward to offset future earnings.

Consider a fund that purchased an asset for $300,000. At 30 June 2026 that asset is worth $200,000. The fund elects the reset, locking in a cost base of $200,000 for Division 296 purposes. The $100,000 loss relative to the original purchase price is permanently locked out of the Division 296 calculation and cannot be carried forward or recovered.

This is distinct from ordinary capital losses under Division 296, which may still carry forward under the usual rules.

The cost base reset is a one-time opportunity, and your decision hinges on two dates:

Before 30 June 2026, you should:

Please speak with your adviser to discuss whether resetting cost bases is suitable for you. It is important to consider multiple outcomes as the election cannot be revoked once made.

This article was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

The information contains projections and forecasts (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group and its related entities make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information. Results are only estimates, the actual amounts may be higher or lower. We cannot predict things that will affect your decision, such as changing interest rates. Seeking professional personal advice is highly recommended before acting on any such assumptions. Past performance is not a reliable indicator of future performance.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.