Division 296 and death benefits: what surviving spouses need to know

Much of the Division 296 discussion focuses on living, planning investors. But its interaction with death benefits is one of its most overlooked dimensions. When a spouse passes away, their superannuation typically flows to the surviving partner and that transfer can push the survivor’s total superannuation balance (TSB) above the $3 million threshold, creating an ongoing annual tax liability they never previously faced.

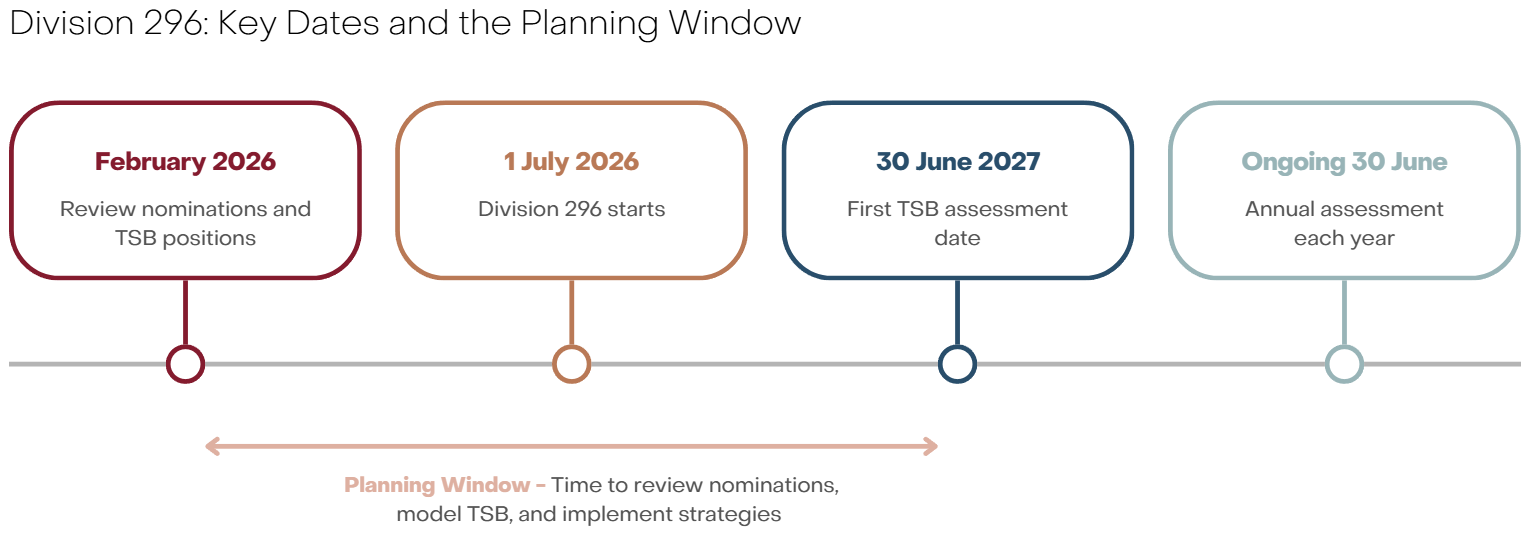

Division 296 will apply from 1 July 2026, with the first TSB assessment at 30 June 2027. That gives couples a genuine planning window, but the lead time required for estate planning changes means the conversation should begin now.

How Division 296 is triggered on a death benefit

Division 296 tax is assessed on an individual’s TSB at 30 June each year. When a death benefit is received, the surviving spouse’s TSB increases often substantially. If that increase pushes their TSB above $3 million, Division 296 will apply to their earnings on the excess from that point forward.

This is not a one-off tax on the inheritance itself. It is an ongoing annual liability on future earnings within super, applying to the portion of the balance above the threshold each year.

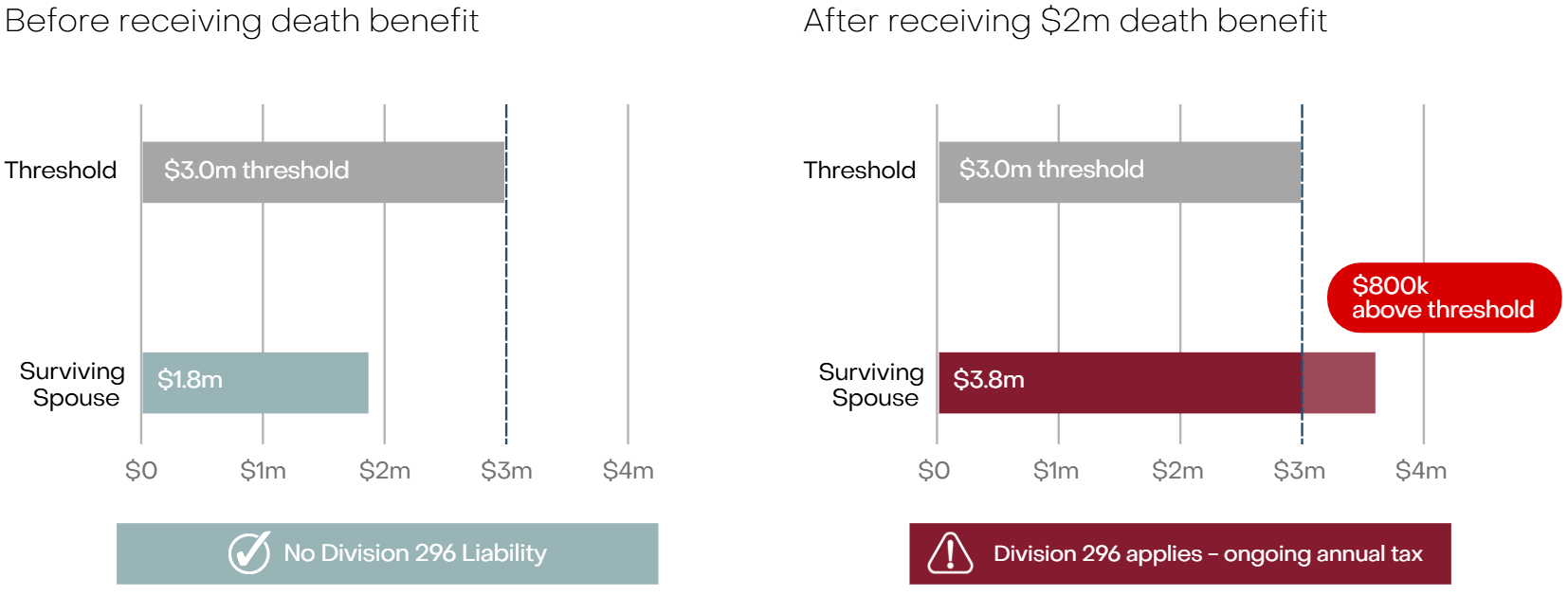

In the example below, a surviving spouse with $1.8 million in super receives a $2 million death benefit. Their TSB rises to $3.8 million placing $800,000 above the threshold. Each year, Division 296 tax will apply to the earnings attributable to that excess.

Source: Evans and Partners

Defined benefit schemes: an added layer of complexity

For members of defined benefit schemes, including Commonwealth public servants with PSS or CSS entitlements, the interaction with Division 296 is more complex. A reversionary pension from a defined benefit fund does not have a straightforward account balance. For TSB purposes, a notional value must be calculated.

The government has indicated this calculation will change under Division 296, moving to a method that takes into account variables such as age, gender, and reversionary status, rather than the existing approach. Until the final rules are settled, modelling the precise impact on a surviving spouse remains difficult.

What is clear is that the notional value of a reversionary pension will count toward the survivor’s TSB and could be substantial. Anyone with a defined benefit entitlement — or whose spouse holds one — should plan to seek specific advice once the final legislation is published.

Timing and the 30 June measurement date

TSB is measured at 30 June each year. A death benefit received and counted before 30 June will be included in the survivor’s TSB at that date, which then informs the following financial year’s Division 296 assessment. With Division 296 commencing on 1 July 2026, the first relevant measurement date will be 30 June 2027.

This sequencing has practical implications for estate administration. In most cases, the timing of benefit payments will be driven by legal, fund and family considerations rather than tax alone. Your adviser can help you understand how these timing mechanics apply to your specific fund and circumstances.

Source: Evans and Partners

What you should be thinking about now

The planning window is real but not unlimited, particularly for changes to binding nominations, defined benefit planning, and SMSF documentation, which take time to implement properly. Here are the key areas to review with your adviser.

Key areas to review with your adviser include:

- Whether your binding death benefit nominations are still appropriate in a Division 296 environment.

- Your combined super position as a couple, and whether a surviving spouse would exceed $3 million if they received the full benefit.

- The presence of any defined benefit entitlements, and how these are likely to be treated once the new valuation rules are finalised.

- For SMSF members, whether the trust deed, pension documents and estate instructions reflect how you want benefits paid on death.

- Whether your super balances are structured in a way that helps manage the Division 296 impact on the surviving partner.

- How your death benefits are directed more broadly, and whether the current approach still makes sense in light of these rules.

Division 296’s intersection with estate planning is one of the more nuanced aspects of the legislation, and one where individual circumstances, combined super balances, fund types, age, beneficiary structures, make a significant difference to outcomes.

The starting point is understanding your combined position and how benefits are directed on death. Talk to your Evans and Partners adviser to understand how Division 296 may affect your household and what steps make sense for your situation.

Disclaimer

This article was prepared by Evans and Partners Pty Limited AFSL 318075. Any advice is general advice only and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Any taxation information is general and should only be used as a guide. The proposed Division 296 legislation has not yet been finalised; this article reflects publicly available information as at February 2026. The defined benefit TSB calculation methodology referenced is subject to further government consultation and has not yet been legislated.

Internship Program - Expression of Interest

Fill out this expression of interest and you will be alerted when applications open later in the year.

Help me find an SMSF accountant

Begin a conversation with an accountant who can help you with your self-managed super fund.

Media Enquiry

Help me find an adviser

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to insights

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Start a conversation

Reach out and start a conversation with one of our experienced team.

Connect to adviser

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.