Division 296: Why balance matters for couples

Division 296 is often discussed as a personal tax problem. But if you’re part of a couple, it’s really a household question and how your combined superannuation is structured could make a significant difference to what you pay.

With a start date of 1 July 2026, now is the time to review your position with your adviser.

How it works

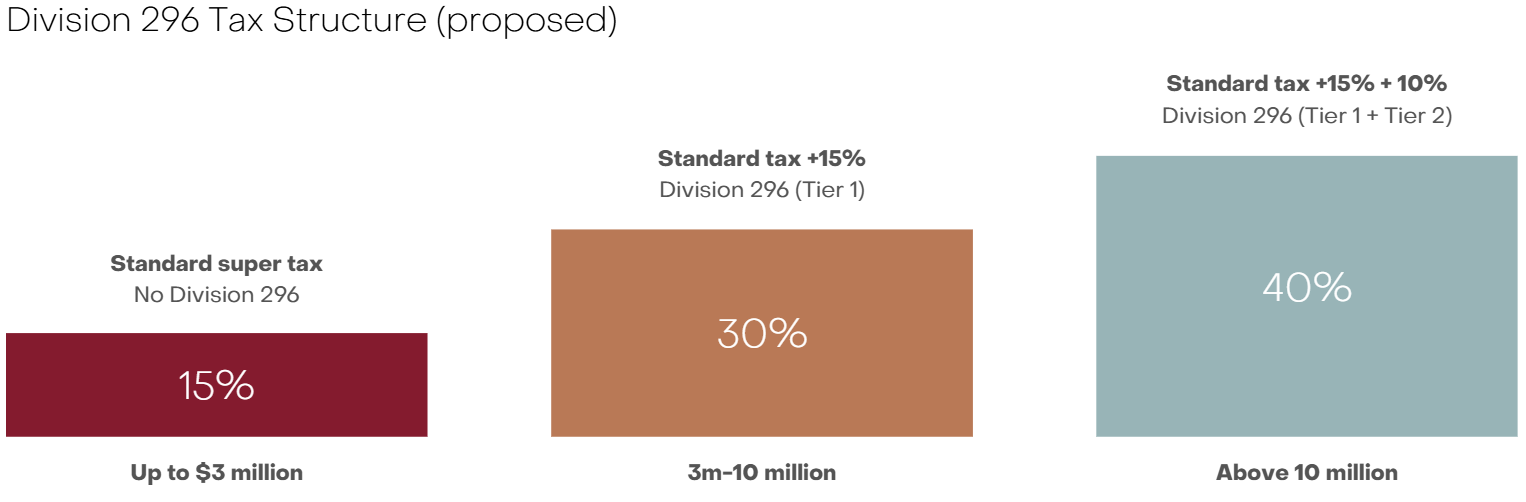

Under the legislation, an additional 15% tax applies to superannuation earnings attributable to balances above $3 million. This brings the effective rate on those earnings from 15% to 30%. For balances above $10 million, a further 10% applies, that’s a combined rate of 40% on that portion.

Source: Evans and Partners

Critically, the $3 million threshold is assessed per person, not per household. A couple can collectively hold up to $6 million in super before either partner becomes liable for Division 296 provided the balances are reasonably equal.

The household opportunity

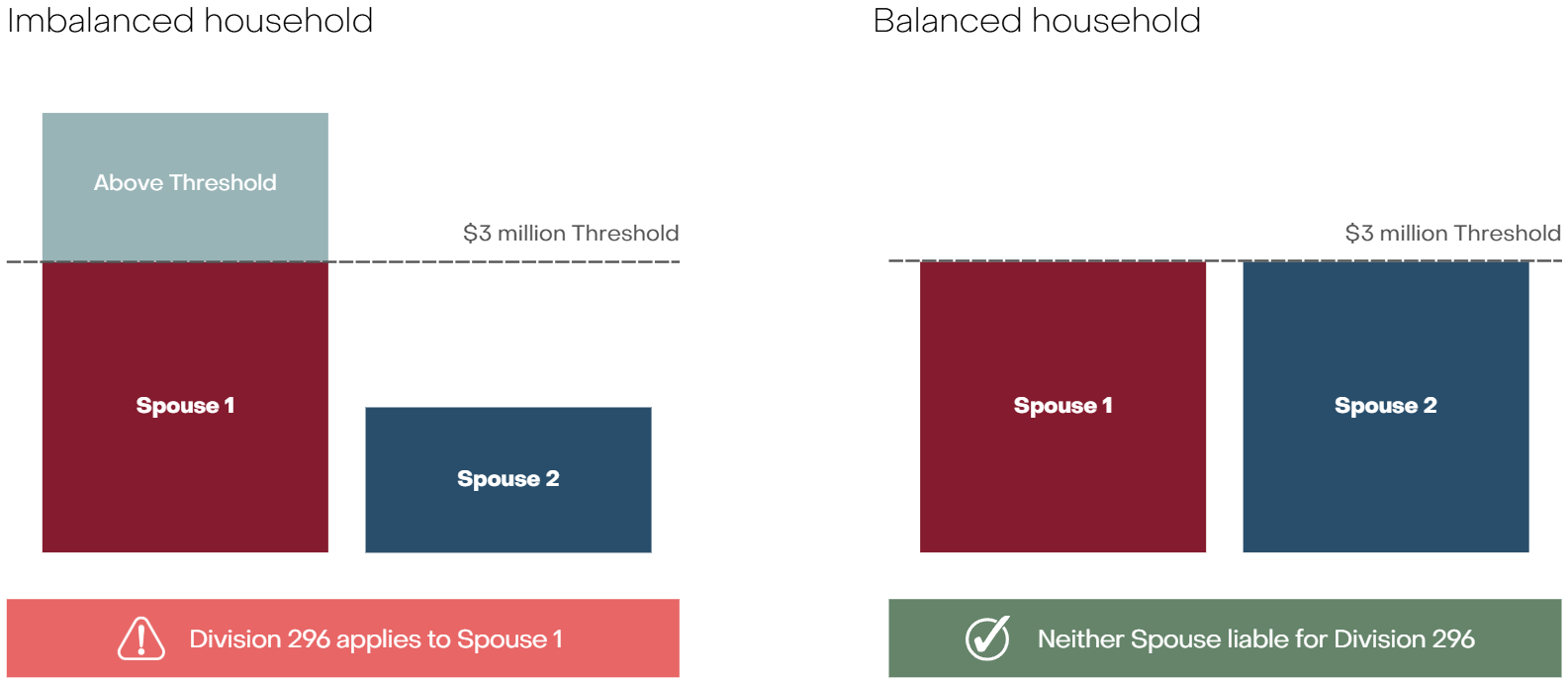

Consider a couple where one spouse holds a significantly larger super balance than the other. Even if their combined total sits well above $3 million, only the partner whose individual balance exceeds the threshold is liable for Division 296 — and only on their earnings above that amount.

Now consider the same household after rebalancing. With each spouse’s balance at or below $3 million, neither is liable — despite the household holding the same total amount in super. The difference in annual tax can be meaningful, and it compounds over time.

Source: Evans and Partners

Earnings for Division 296 are based on fund earnings — broadly, taxable income adjusted for contributions and exempt pension income. This includes realised capital gains but excludes unrealised paper gains, giving couples genuine control over the timing of when gains are recognised.

Strategies to explore

The right approach will depend on your age, contribution eligibility, and estate planning needs and not all strategies will be appropriate for every couple. These are worth discussing with your adviser to understand what applies to your situation.

Broadly, the options available fall into a few categories.

Contribution management: For couples still accumulating, existing super rules allow future contributions and growth to be directed toward the lower balance partner over time. This might involve adjusting who makes concessional and non-concessional contributions, and in what order, considering each partner’s remaining cap space and eligibility.

Pension and withdrawal structuring: For those already in, or approaching, retirement, how and when money moves between accumulation and pension phases can change overall tax outcomes, including Division 296 exposure. In some cases this may involve adjusting pension commencement amounts, the level and source of withdrawals, or how re‑contributions are managed between partners, recognising that every approach has trade‑offs around contribution caps, capital gains, and liquidity.

Longer-term considerations

Rebalancing isn’t without trade-offs. Moving money between accounts or super funds may trigger capital gains tax within the fund, and contribution caps limit how quickly balances can shift. The $3 million threshold also indexes with CPI over time, which gradually changes the equation.

Estate planning matters here too. Inherited super counts toward the surviving spouse’s balance and can push someone into Division 296 territory unexpectedly. This makes it worth consider how funds are structured and directed as part of the broader plan.

The Treasury Laws Amendment (Building a Stronger and Fairer Super System) Bill 2026 has been tabled, and the primary legislation is progressing. Supporting regulations across several areas including defined benefit valuations and attribution methodology are still pending. We suggest focusing on strategies that make sense regardless, rather than waiting for every detail to be resolved.

The starting point is understanding your combined position. Talk to your Evans and Partners adviser to understand how Division 296 may affect your household and what steps make sense for your situation.

Disclaimer

This article was prepared by Evans and Partners Pty Limited AFSL 318075. Any advice is general advice only and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Any taxation information is general and should only be used as a guide. The proposed Division 296 legislation has not yet been finalised; this article reflects publicly available information as at March 2026.

Internship Program - Expression of Interest

Fill out this expression of interest and you will be alerted when applications open later in the year.

Help me find an SMSF accountant

Begin a conversation with an accountant who can help you with your self-managed super fund.

Media Enquiry

Help me find an adviser

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to insights

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Start a conversation

Reach out and start a conversation with one of our experienced team.

Connect to adviser

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.