Financial Planning

Under the Budget proposal, the key date for negative gearing is 7:30pm AEST on 12 May 2026. Residential properties held at that time, including properties under contract but not yet settled, are grandfathered. Investors in this position retain the ability to offset rental losses against their other assessable income, such as salary, for as long as they hold that property. Their existing deductibility remains unchanged under the negative gearing reforms.

The position is different for established residential properties acquired after that time. From 1 July 2027, losses from those properties can only be offset against rental income or capital gains from other residential property. Losses that cannot be used in a given year are carried forward and may be applied against residential property income in future years. Critically, they cannot be applied against wages, business income or broader investment returns.

For investors holding multiple properties across different acquisition dates, the portfolio would operate under two different sets of rules simultaneously.

The CGT changes require careful attention to timing. The 50% CGT discount is proposed to be replaced from 1 July 2027 by cost base indexation, combined with a minimum 30% tax on net capital gains. However, transitional rules preserve the discount for gains accrued before that date.

For investors who purchased before 1 July 2027 and sell after that date, the gain is effectively split at the transition point. The gain accrued up to then, calculated as the difference between the original cost base and the property’s market value, remains eligible for the 50% discount. Only the gain accruing after that point would be subject to the new indexation and minimum tax regime.

The valuation of the property at 1 July 2027 is a critical variable. Investors may use either a formal market valuation or a specified apportionment formula based on the asset’s growth rate over the holding period. The choice of method may materially affect the tax outcome on sale. In the absence of an arm’s length transaction at that date, valuations may be open to scrutiny.

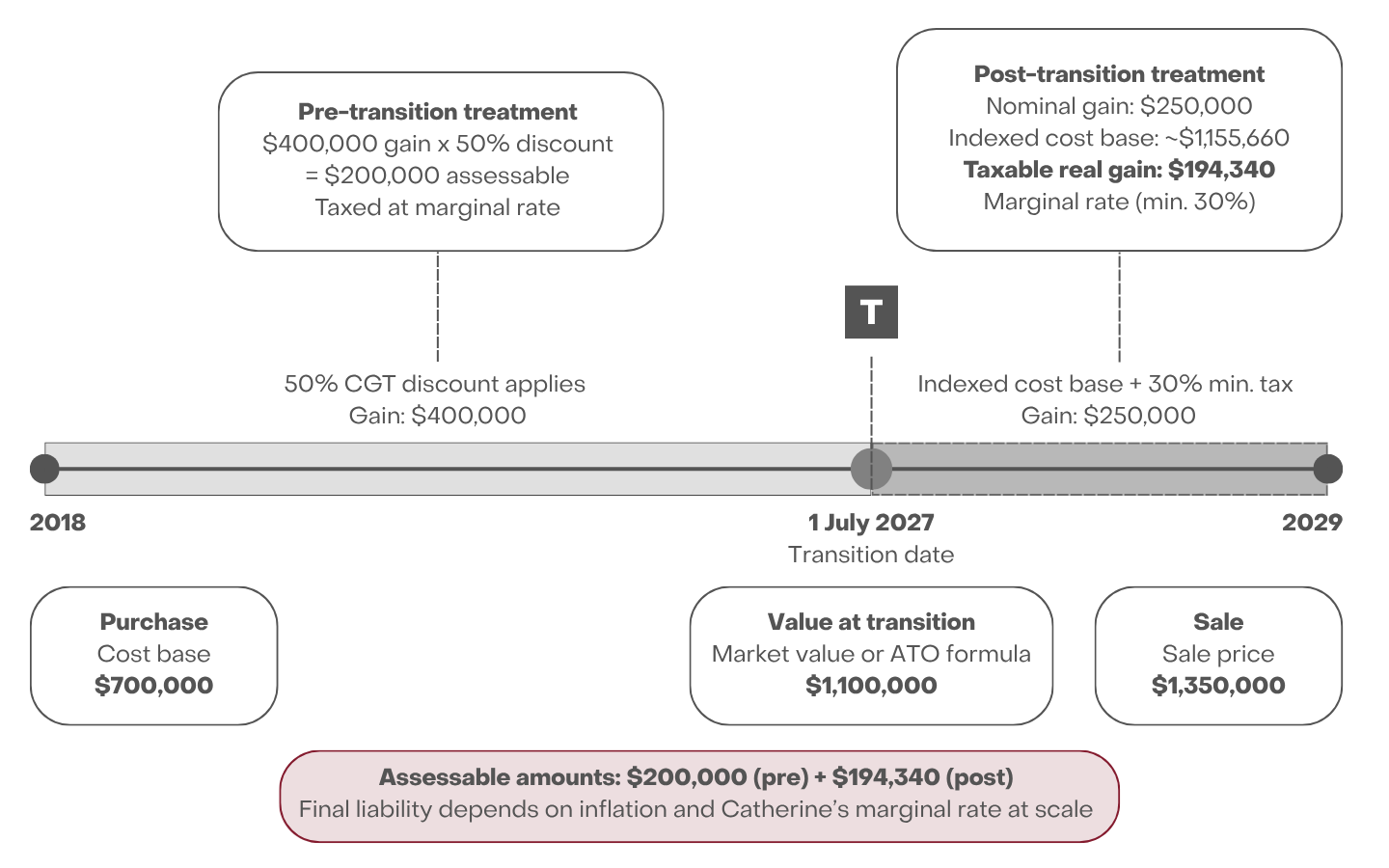

Catherine purchased an established investment property in 2018 for $700,000. By 1 July 2027, its market value has grown to $1,100,000. She sells in 2029 for $1,350,000.

On the pre‑transition gain of $400,000, Catherine is eligible to apply the 50% CGT discount, bringing the assessable amount to $200,000. For the post‑transition period, Catherine has a nominal gain of $250,000, however this amount is not taxed directly. Instead, the 1 July 2027 value of $1,100,000 becomes the new cost base and is indexed for inflation over the two years to sale. Assuming inflation of 2.5% per annum, the indexed cost base becomes approximately $1,155,660, resulting in a taxable real gain of $194,340. Tax is then applied to this amount at Catherine’s marginal rate, subject to a minimum 30% tax rate.

The combined tax outcome is materially different from what would have applied had the full gain been assessed under either the old or new rules alone, with the final liability influenced by both inflation and Catherine’s marginal tax rate in the year of sale.

Illustrative example only.

For investors who have owned established investment properties for many years, the transitional CGT rules largely protect what has already been built. Gains to date remain eligible for the 50% discount, with the new tax burden applying only to growth from 1 July 2027 onward.

The more relevant question is how the loss of broad negative gearing deductibility for properties acquired after 12 May 2026 changes the cash flow assumptions behind an investment strategy. For grandfathered properties, those assumptions remain intact. For any subsequent acquisitions, they do not.

For most investors, what you already own continues much as expected. What you buy next needs to work without relying on the same tax settings.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.