Financial Planning

Biotech and healthcare investing is unlike almost any other sector, and for good reason.

The most fundamental thing to understand about biotech is that value doesn’t build gradually the way it might in a bank or a retailer. Instead, it accrues in steps as companies hit clinical milestones and progressively de-risk their programs. A company moving from Phase 1 to Phase 2 trials, or receiving regulatory approval, can see its valuation jump dramatically overnight. This means patience is essential, and so is a clear-eyed understanding of what risks remain on the path ahead.

This requires a five-factor lens: biology (does the science work?), execution (can management actually run the trials and manufacture the product?), capital (will they survive long enough?), competition and reimbursement (will anyone pay for it?), often overlooked is the potential for clinical uptake. That last one is the most human of all: will doctors actually want to prescribe it to their patients? If there’s genuine pull from clinicians, that can be enormously powerful.

Biotech and medtech are quite different beasts, though they’re often lumped together. Biotech is biology-risk dominant — it lives or dies on clinical data, P-values, and regulatory pathways. Medtech, on the other hand, is more about execution: does it fit into clinical workflows, will hospitals pay for it, and can you scale adoption? Australia actually has some real strengths in medtech, with deep engineering capability and strong clinical trial infrastructure. For biotech, it’s a more complicated picture.

Australian biotech companies tend to be earlier-stage than their US counterparts. The domestic healthcare market simply isn’t large enough to commercialise most innovations locally, so companies need global ambition from day one. In the US, there’s much greater capital abundance, later-stage IPOs, and more patient tolerance for long evidence cycles. Europe leans on grants and tends to move more slowly to market. Australia’s challenge isn’t the quality of the science — we punch well above our weight there — it’s access to capital and the patience required to see complex programs through. The “Valley of Death,” the gap between promising research and commercial reality, is real and well known here.

In terms of what’s interesting right now, there has been a clear shift in market appetite away from pure science stories and towards execution stories with near-term revenue visibility. Devices and diagnostics are gaining favour over longer-cycle therapeutics, and the market increasingly wants to know not just “does it work?” but “how do we get paid for this?” There’s also growing interest in pragmatic trial designs and minimally invasive procedures that can save hospitals money — innovations that deliver both clinical and economic benefit are commanding a premium.

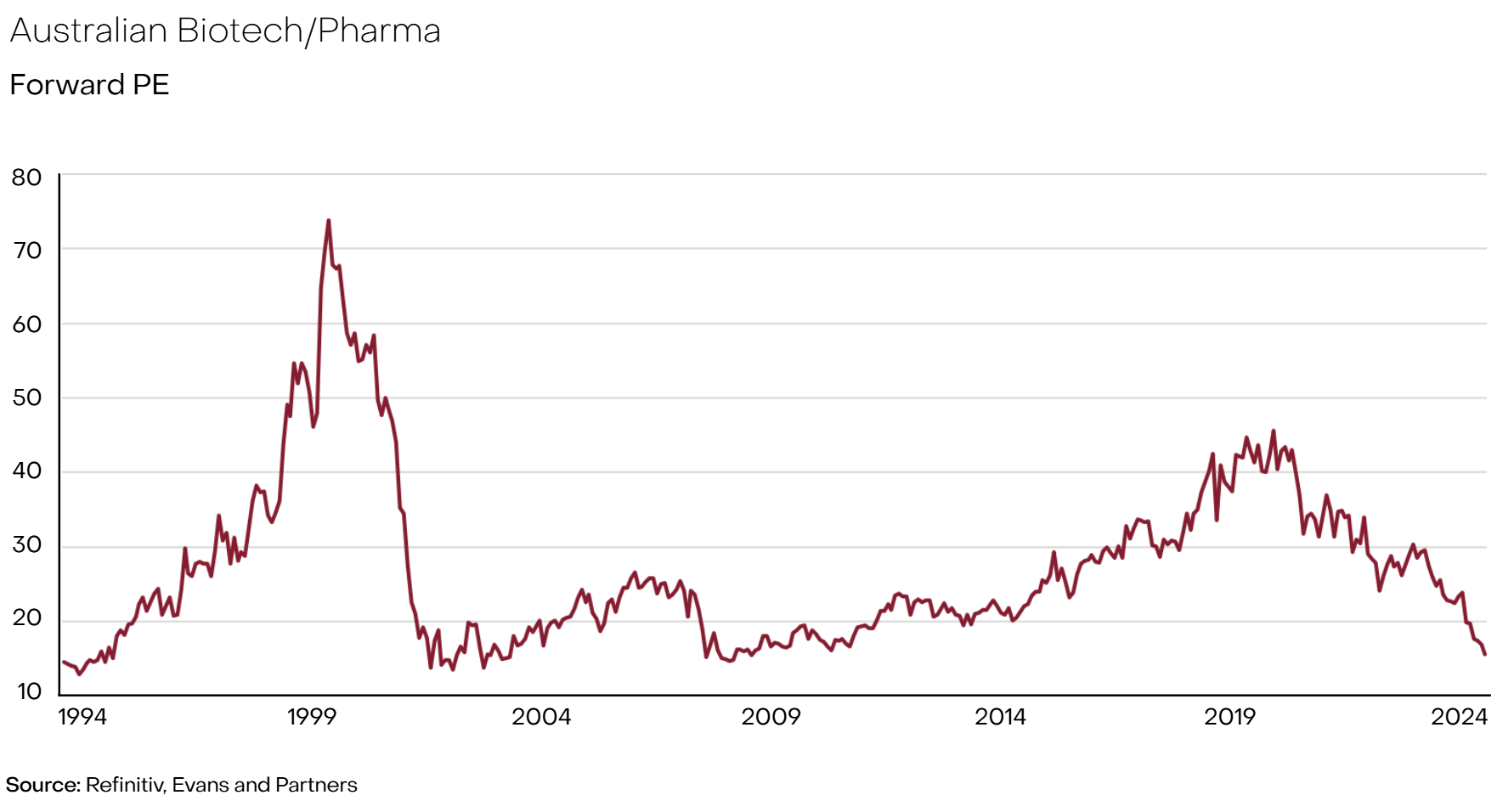

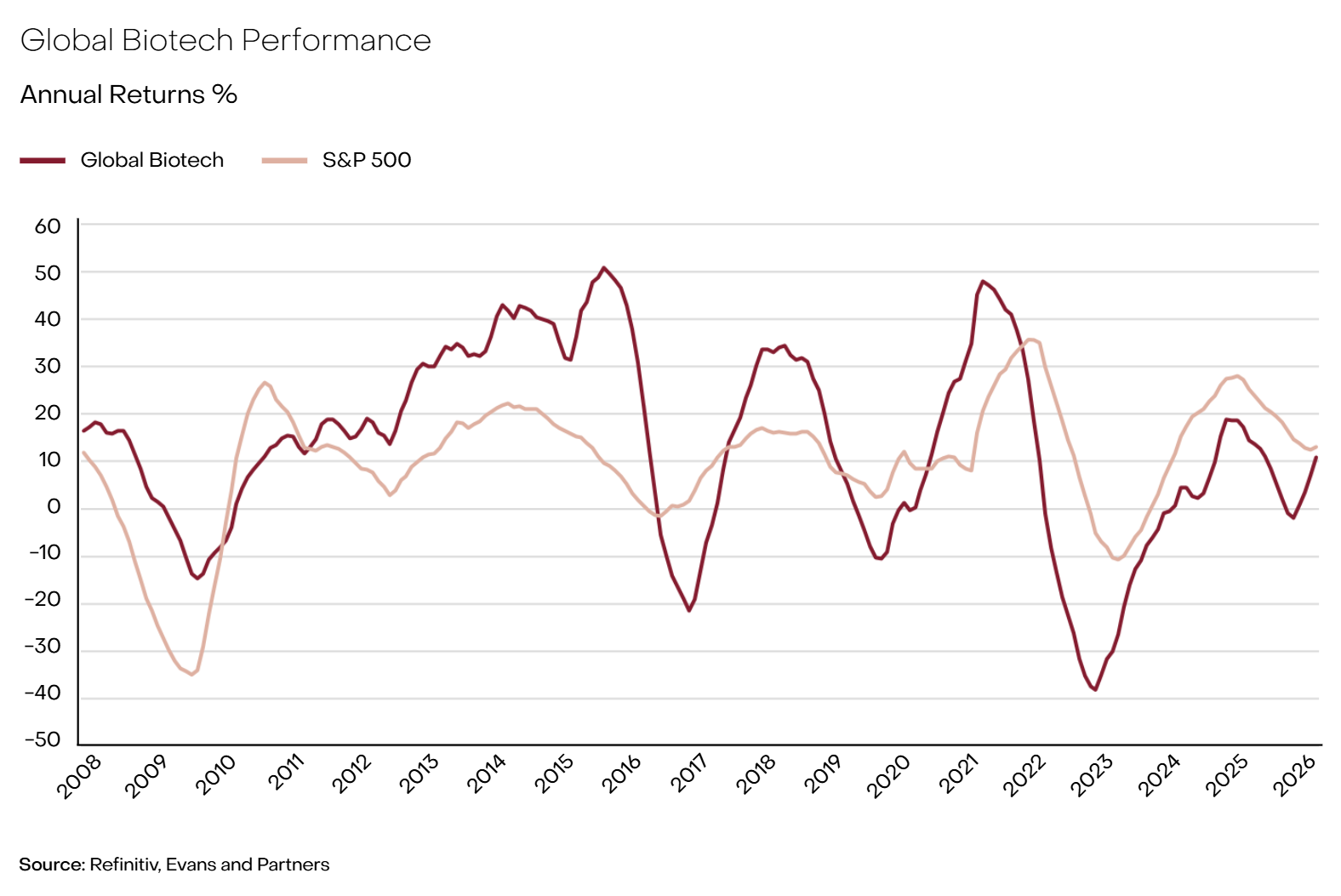

As for timing, the biotech sector has been through a long, harsh nuclear winter, but there are signs of an upward trend, supported by deal activity and the emergence of major thematic tailwinds — particularly GLP-1 drugs and AI’s growing role in drug discovery. Neither of those are short-term phenomena, and Australia is well positioned to participate.

The key message for investors is diversification. Biotech is genuinely a portfolio game. Unless you have deep, specific insight into a particular technology or management team, picking a single name is more like speculation than investing. A portfolio approach, combined with rigorous attention to the risk profile of each company rather than just the blue-sky revenue potential, is the approach most likely to generate strong long-term returns.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

This communication is not intended to be a research report (as defined in ASIC Regulatory Guides 79 and 264). Any express or implicit opinion or recommendation about a named or readily identifiable investment product is merely a restatement, summary or extract of another research report that has already been broadly distributed. You may obtain a copy of the original research report from your adviser.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.