Financial Planning

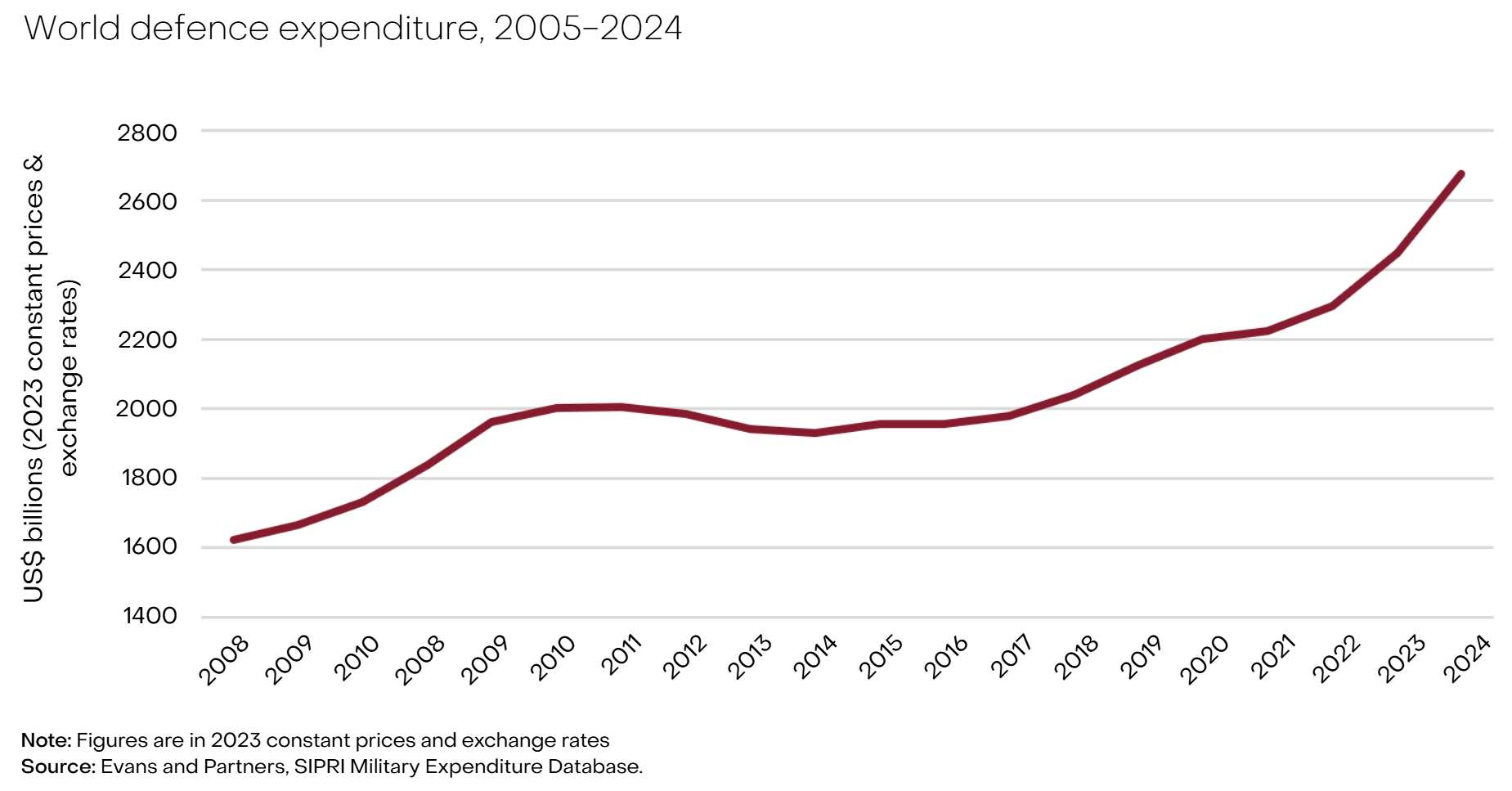

The world is rearming. According to the IISS Military Balance, global defence spending reached a record US$2.63 trillion in 2025, with analysts projecting it will exceed US$3 trillion by year-end and US$3.6 trillion by 2030. Europe’s share has climbed from 17% to 21% in just three years, NATO has committed to a 5% GDP target, and the US defence budget is set to surpass US$1 trillion in 2026.

This flow of capital is creating significant investment and economic opportunity — but it comes with human context. War exacts enormous social and humanitarian costs, and the UN Secretary-General’s 2025 report noted that rising military expenditure has coincided with both deteriorating global security and declining progress toward the Sustainable Development Goals — in part due to the diversion of public resources away from healthcare, education and other essential services. This raises a key question. How should a ‘responsible’ investor approach the defence sector?

An emerging industry framework

This is a complex area with no single right answer, but across the global investment industry a broad tiered approach is taking shape — distinguishing between what should remain firmly excluded, what requires enhanced scrutiny, and where disciplined engagement is appropriate.

The EU’s 2025 Defence Omnibus, the UK FCA’s clarifying statement, and initiatives such as the new Guidance for Responsible Investment in Defence (GRID) — being developed by a coalition including Schroders, Amundi and the Church Commissioners — are all reinforcing this structure.

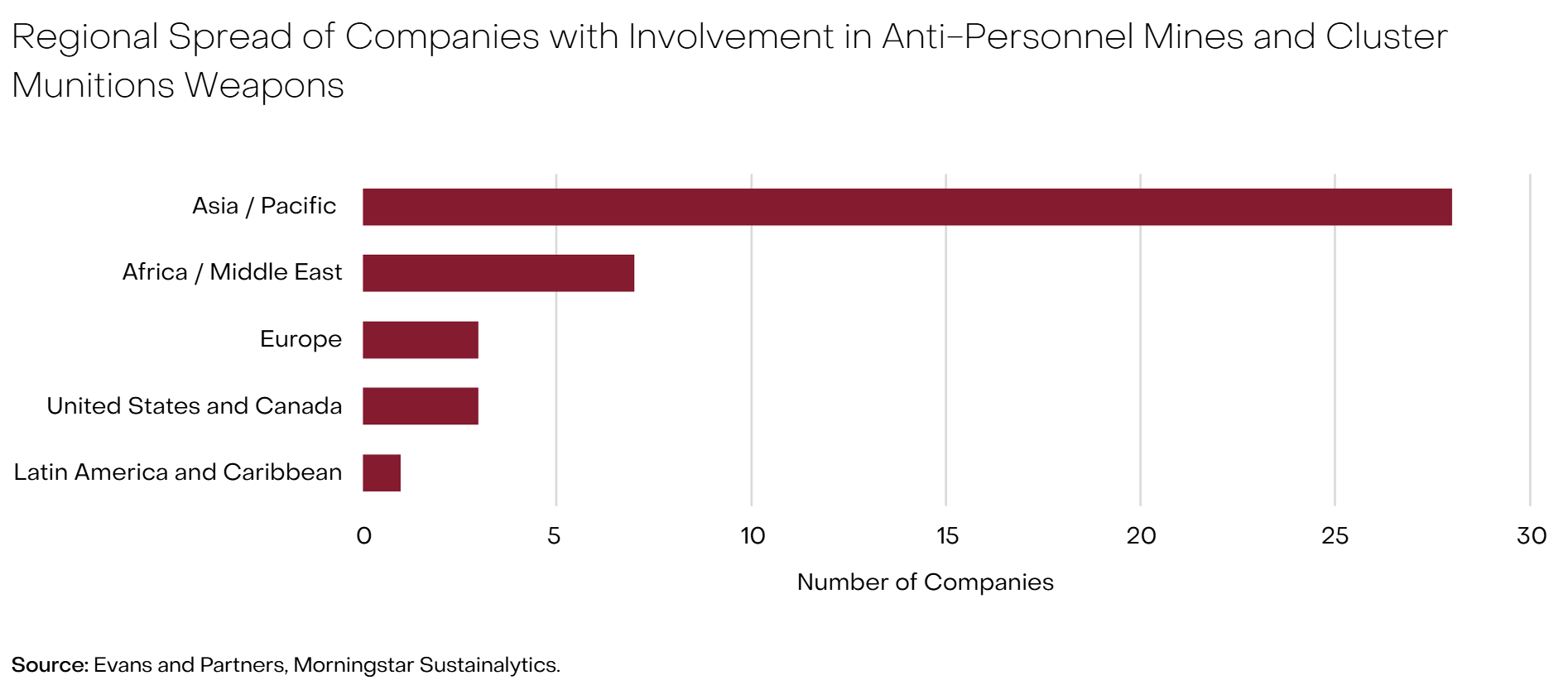

First — exclude controversial weapons. The term ‘controversial weapons’ refers to weapons prohibited or heavily restricted under international conventions because of their indiscriminate and long-lasting impact on civilian populations. This typically includes anti-personnel mines, cluster munitions, and chemical and biological weapons. These weapons are excluded because their effects cannot be reliably confined to military targets — unexploded cluster submunitions, for example, can kill civilians for decades after a conflict ends. Zero-tolerance exclusion is now standard practice across ESG-focused portfolios globally.

Second — apply enhanced scrutiny. Nuclear weapons, depleted uranium and white phosphorus sit in more contested territory. These are not classified as ‘prohibited weapons’ under the EU’s updated framework, and several major European investors have recently reintegrated weapons manufacturers in their portfolios. However, they remain excluded under many institutional policies, including Responsible Investment Association Australasia (RIAA) certification in Australia. Investors should assess the nature of involvement, the company’s trajectory, and whether manufacturers are expanding or proactively exiting.

Third — engage. It is worth recognising that defence is not solely about weapons. The modern defence sector encompasses cyber security, satellite communications, logistics, infrastructure and intelligence — much of it with dual civilian-military application. There are also legitimate ethical arguments around a nation’s right to self-defence; Ukraine’s defence against invasion is a case in point. Companies providing these capabilities can be appropriate holdings, but require active ESG scrutiny – and direct engagement from investors on these issues.

Defence has performed strongly and carries genuinely defensive financial characteristics — stable government contracts, high barriers to entry, and structurally growing demand. Its supply chains are also materials-intensive, with copper, aluminium, titanium, rare earths and steel all critical inputs — reinforcing an already tight commodity picture alongside electrification and the energy transition. For investors, the opportunity is real. But so is the complexity. Sector-specific responsible investment guidance is only now being developed, and until those frameworks mature, investors will need to do their own work — clear and defined exclusions, active company engagement, and transparency around their approach.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

This communication is not intended to be a research report (as defined in ASIC Regulatory Guides 79 and 264). Any express or implicit opinion or recommendation about a named or readily identifiable investment product is merely a restatement, summary or extract of another research report that has already been broadly distributed. You may obtain a copy of the original research report from your adviser.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.