Financial Planning

Australian women retire with less superannuation than men. Not because they are less capable of building wealth, but because the system and life itself have historically stacked the odds against them. International Women’s Day may have passed for another year, but the conversation it sparks around women’s financial security doesn’t have to stop there. The opportunity to act exists year-round.

The gap is closing, but the pace matters. Understanding the drivers, and the practical steps available right now, can make a significant difference.

According to the Australian Taxation Office (ATO), women aged 60 to 64 retire with a median super balance around 21% lower than men. This shortfall has real consequences: less capacity to cover everyday expenses, fewer resources to absorb the unexpected, and greater reliance on external income in retirement.

$163,218

Median super balance (women, age 60–64)

$219,773

Median super balance (men, age 60–64)

21.3%

Gender super gap (national average)

Source: ATO Tax Statistics 2024; 2025 Status of Women Report Card.

What is less widely understood is the role of discretionary pay. WGEA’s (Workplace Gender equality Agency) 2025 data shows men earn, on average, 60% more than women from bonuses, allowances, and overtime and these flow directly into super balances. Salary alone undersells the real gap. Two compounding realities make the picture harder. Women retire earlier on average, at 62.7 years compared to 64.9 for men, and they live longer. A smaller balance, stretched over more years, leaves less room for the unexpected.

The drivers behind the gap are consistent: career breaks for caring responsibilities, part-time work, a gender pay gap, and a tendency to invest conservatively. Each factor compounds the others over a working life. Systemic reform is underway, including superannuation being paid on government-funded parental leave since 1 July 2025 which could leave a mother-of-two $12,500-$14,500 better off at retirement. But structural change alone will not close the gap quickly enough for women who are working and saving right now.

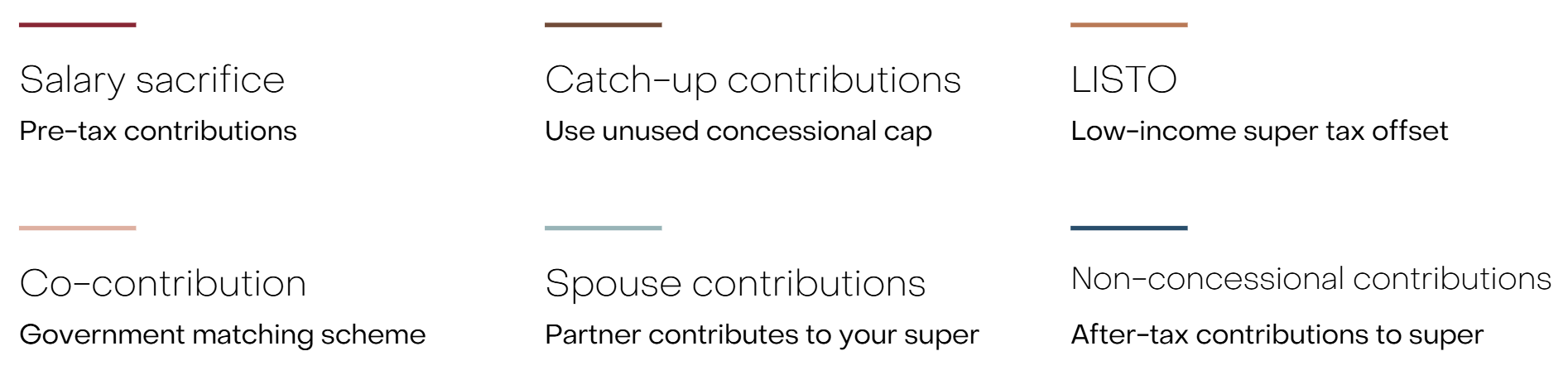

Super remains one of the most tax-effective vehicles to build wealth over the long term. With several contribution options available, it is often worth exploring more than one to find the combination that suits your situation.

Contribution eligibility depends on individual circumstances including age, total super balance, and taxable income. It’s important to get professional advice before acting.

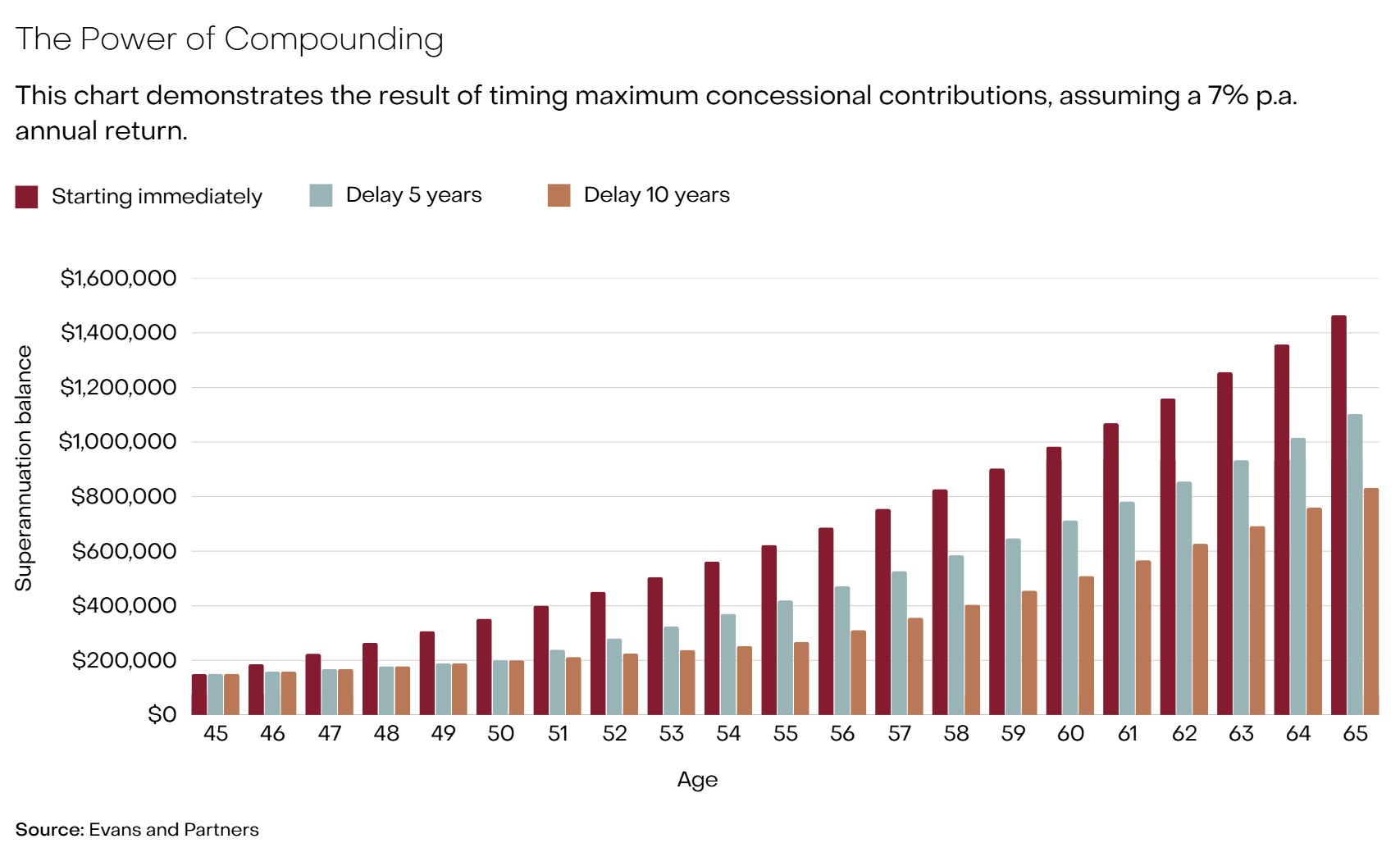

Super rewards consistency and time above all else. Even modest additional contributions, made regularly, can grow into a meaningfully different retirement outcome.

Delaying contributions by five years could cost around $362,000 at retirement. Wait ten years and that figure rises to $633,000. For women who already face a structural super disadvantage, amounts like these can make the difference between financial independence in retirement and relying on external support.

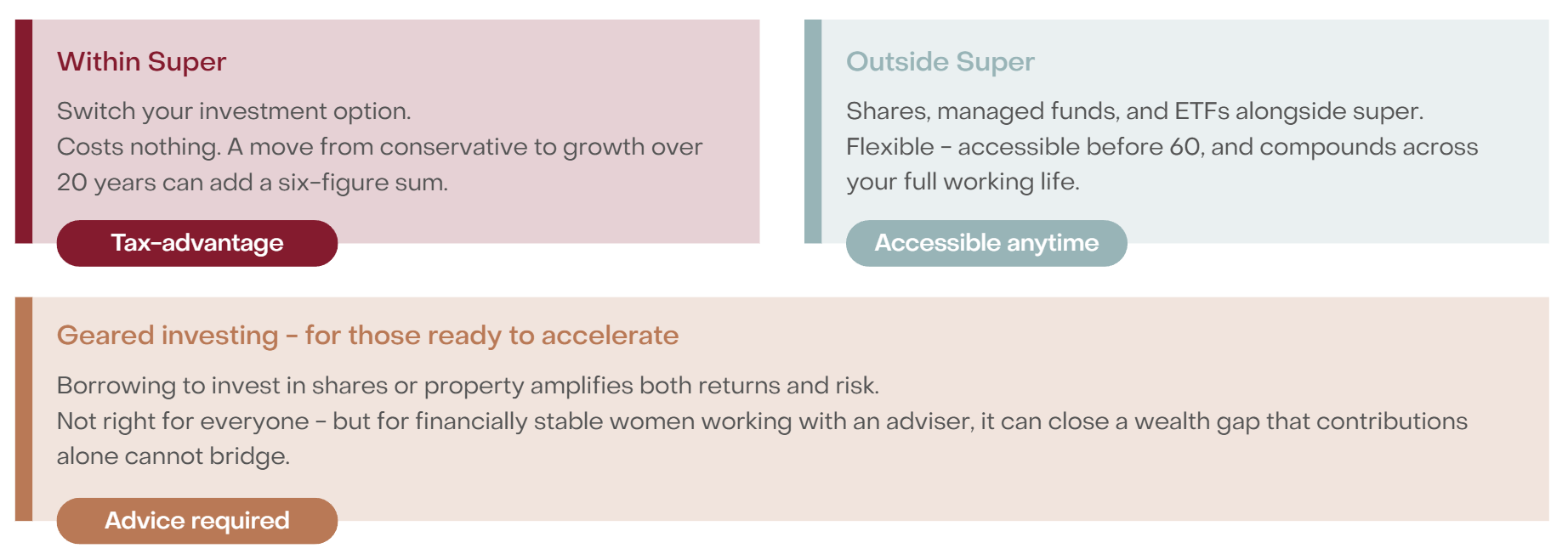

While there is a place for caution as retirement approaches, investment selection should reflect your time horizon. Investment decisions are one of the most powerful and perhaps most underused levers available to women building wealth. There are three distinct dimensions worth considering.

The right investment strategy built around your time horizon, your circumstances, and the options available to you is one of the most powerful steps you can take to close the gap on your own terms.

You don’t need to do everything at once. But knowing where you stand, and aligning your strategy with your goals, puts you firmly in the driver’s seat.

Bringing together a financial adviser, tax specialist, and where relevant a legal adviser ensures your super strategy is both effective and sustainable. Professional guidance helps you identify the right contribution mix, optimise your investment option, and plan around career transitions without losing ground.

Just as importantly, a good adviser ensures flexibility, so your strategy can adapt as your income changes, your goals evolve, or legislation shifts, without compromising your financial security.

Financial independence in retirement is not a given. But with the right steps, taken early and consistently, it is well within reach.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

This communication is not intended to be a research report (as defined in ASIC Regulatory Guides 79 and 264). Any express or implicit opinion or recommendation about a named or readily identifiable investment product is merely a restatement, summary or extract of another research report that has already been broadly distributed. You may obtain a copy of the original research report from your adviser.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.