Financial Planning

At present, conditions for Australia’s major banks have been favourable. The domestic economy has proved resilient, credit quality remains sound, and the banks have delivered higher earnings certainty relative to the market. Bank equity valuations reflect this confidence — the major banks have re-rated materially over the past two years and are now trading at historically elevated price-to-earnings multiples.

Banking in Australia looks very different to how it did just two decades ago. Cash once accounted for nearly 70% of transactions; today that figure has fallen to around 13%. Mobile wallet transactions have grown from $7 billion to $160 billion in just six years. Three in four new mortgages are now originated through brokers rather than directly with a bank. These are not incremental changes — they reflect a fundamental transformation in how Australians access and use financial services.

The drivers of this transformation are both technological and global. Digital banks, fintechs, buy-now-pay-later providers, non-bank lenders, and global payment platforms have entered virtually every segment of the banking market, increasing competition and expanding consumer choice. At the same time, Australian banks have become more deeply integrated into global capital markets, relying heavily on offshore wholesale funding to support domestic lending. This has introduced a growing sensitivity to international interest rate movements, currency fluctuations, and geopolitical developments that are increasingly difficult to insulate against.

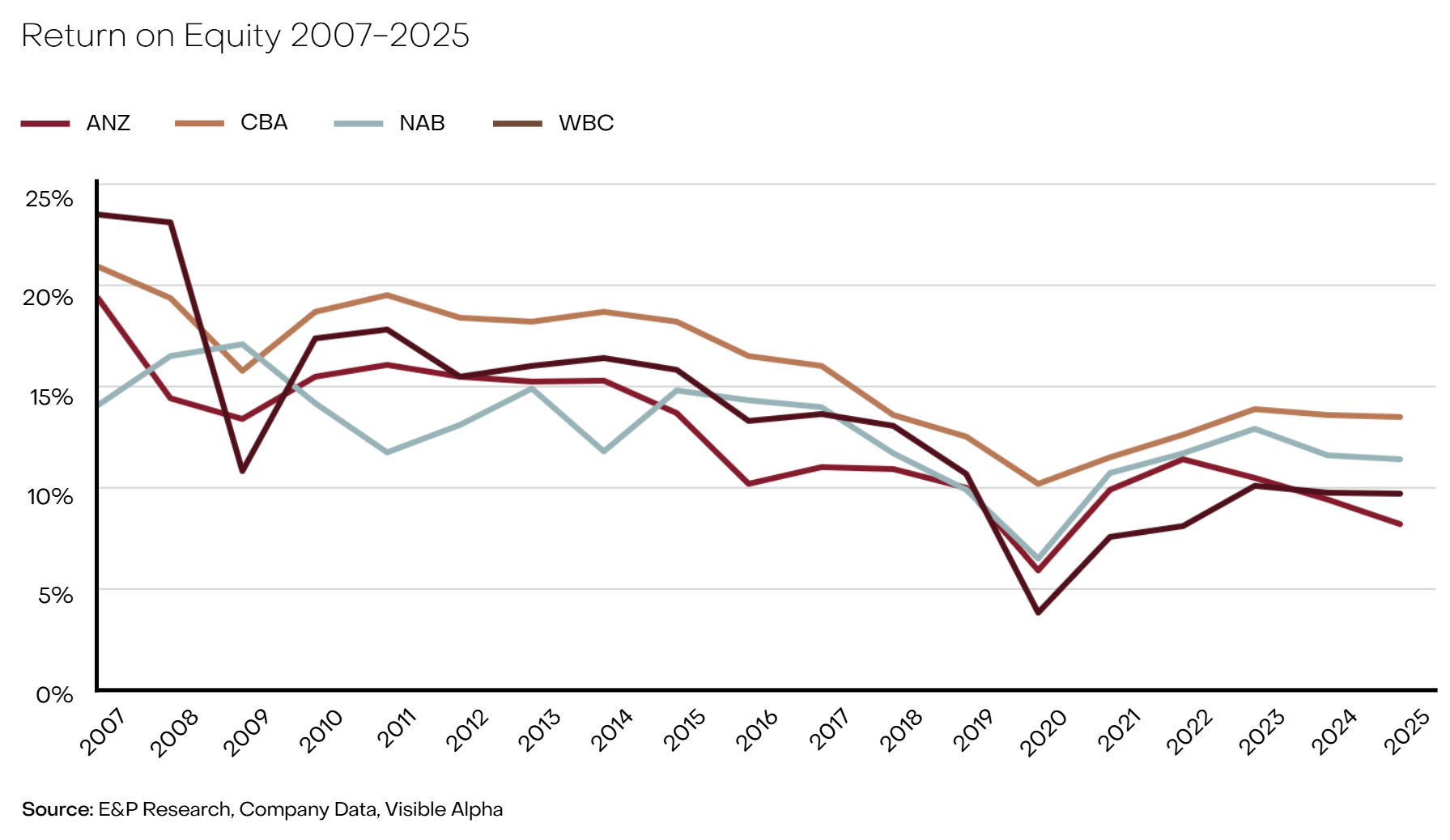

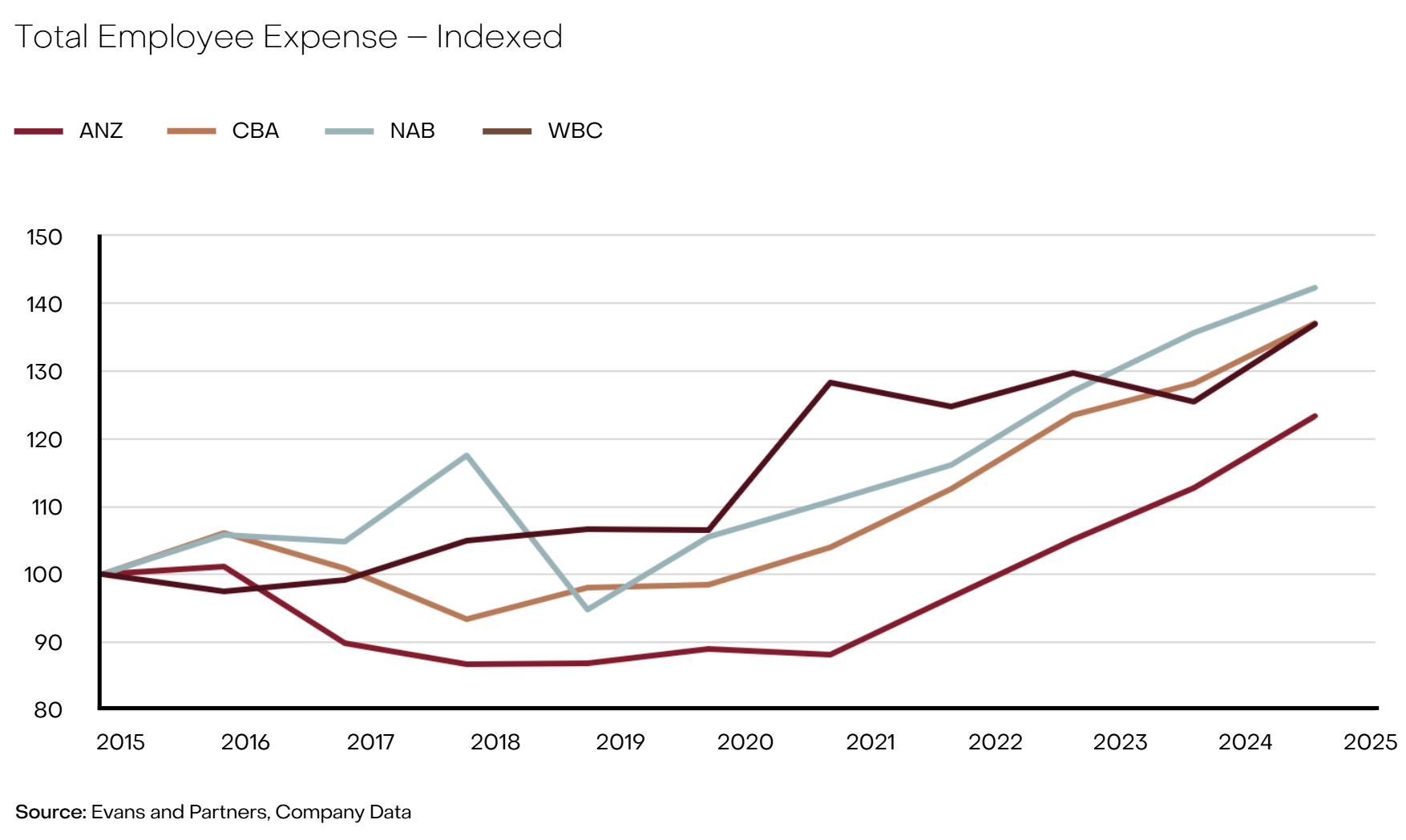

Looking beyond the near-term, however, a more complex picture emerges. The structural forces reshaping banking — technology, globalisation, and evolving regulation — are creating pressures that cyclical tailwinds alone are unlikely to resolve. Competition for deposits and lending continues to intensify as lower-cost digital players expand their market presence. The share of home loans, business lending, and deposits held by the major banks has declined steadily since 2019. Return on equity has fallen by approximately a third over the past decade and now trails comparable banking systems in the UK, US, and Canada. Rising compliance costs — driven by post-Royal Commission obligations, cybersecurity investment, and new payments infrastructure — have pushed cost-to-income ratios higher, pressuring efficiency.

A further structural tension is emerging around the question of regulatory balance. Major banks carry a broad set of community obligations — maintaining regional branches and ATMs, offering low- and no-fee accounts, funding shared payment infrastructure, and meeting the full suite of consumer protection requirements — that newer, lighter-regulated competitors are not required to match. As revenue becomes more fragmented across a growing number of players, the capacity of major banks to fund these services while also building the capital buffers that underpin system resilience deserves close attention.

This matters beyond the banking sector itself. Well-capitalised banks that are able to sustain lending through economic downturns have historically played a critical role in moderating the depth of recessions. Australia’s experience through the Global Financial Crisis — where stronger capital buffers allowed banks to keep credit flowing — stands in contrast to markets where undercapitalised institutions were forced to retrench, deepening and prolonging economic downturns.

With bank equities arguably priced for a continuation of current conditions, investors would be prudent to weigh whether current valuations adequately reflect the structural challenges that lie ahead.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

This communication is not intended to be a research report (as defined in ASIC Regulatory Guides 79 and 264). Any express or implicit opinion or recommendation about a named or readily identifiable investment product is merely a restatement, summary or extract of another research report that has already been broadly distributed. You may obtain a copy of the original research report from your adviser.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.