Financial Planning

The key date is 7:30pm AEST on 12 May 2026. Established residential properties held at that time, including properties under contract but not yet settled, are grandfathered under the previous rules. Clients who already hold established residential property retain their current negative gearing deductions until the property is disposed of.

For established residential property purchased after that date, the position is different. From 1 July 2027, rental losses on those properties can no longer be offset against wages or other unrelated income. Losses can only be carried forward and applied against future residential property income. Newly constructed properties are carved out entirely and remain eligible for negative gearing under the existing rules, as part of the government’s housing supply policy.

Alongside this, the 50% Capital Gains Tax (CGT) discount for assets held longer than 12 months has been replaced with cost base indexation and a 30% minimum tax on net capital gains, effective 1 July 2027. This applies to all asset classes, not just property, and gains accrued before that date remain eligible for the existing discount. New residential dwellings are treated differently. On sale, clients holding these properties can choose between the 50% discount or the new indexation and minimum tax method, whichever produces the better outcome at the time.

Negative gearing itself has not been abolished. What has changed is where losses on new established property can be applied. Negative gearing on shares, ETFs, commercial property, and other investment assets is entirely unchanged, and the deductibility of interest against income from those assets remains available as it always has. For clients who had been relying on a tax deduction from property losses to reduce their salary income, the same outcome remains available, just through a different asset class.

A share portfolio funded by an investment loan works on the same principle. If the interest cost on the loan exceeds the dividend income generated by the portfolio, the resulting loss is deductible against wages and other income, in the same way established property once was.

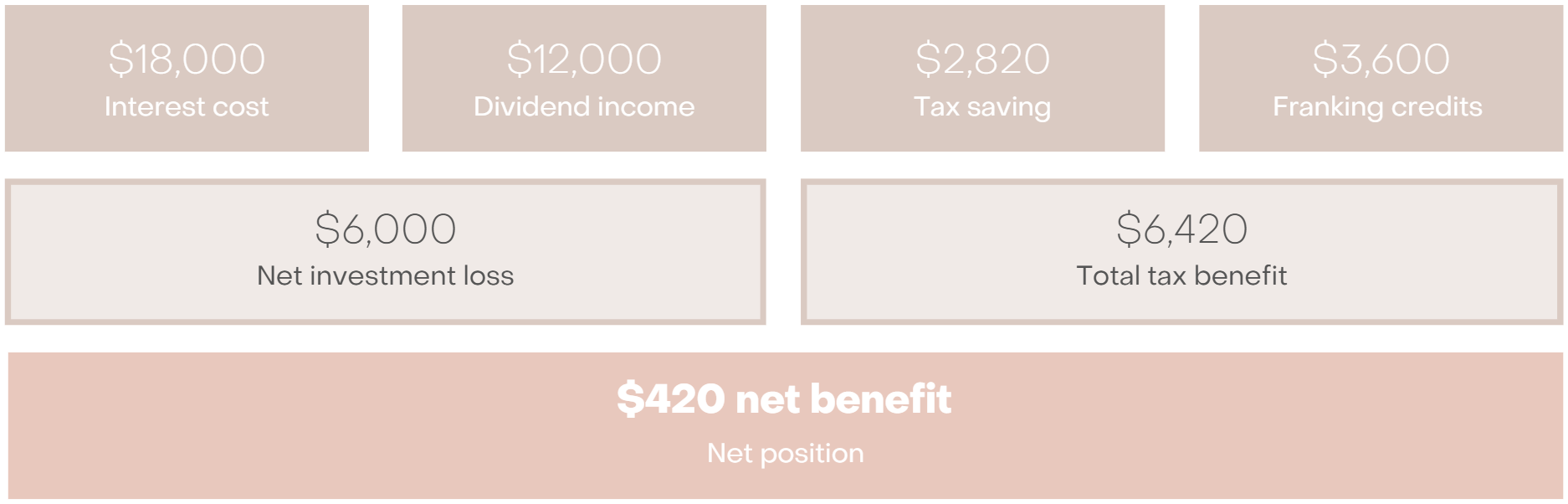

Consider Sophie, who borrows $300,000 at 6% interest, paying $18,000 per year. Her portfolio generates $12,000 in dividend income annually. The net investment loss of $6,000 produces a tax saving of approximately $2,820 at the top marginal rate of 47%, reducing Sophie’s true out-of-pocket holding cost to $3,180.

Franking credits improve the position further. If Sophie’s portfolio carries a 4% dividend yield that is 70% franked, it generates approximately $3,600 in franking credits. For a client with a significant tax liability, those credits offset tax payable dollar for dollar, adding to the benefit already achieved through the deduction.

Debt recycling extends this concept further and suits clients with the right financial foundations already in place. The strategy works by converting non-deductible mortgage debt into deductible investment debt over time. As loan repayments reduce the home loan balance, that equity can be redrawn and directed into income-producing investments, most commonly a diversified share portfolio or ETFs. The redrawn portion is used for investment purposes, so the interest on that amount becomes tax deductible, while the total debt itself does not increase.

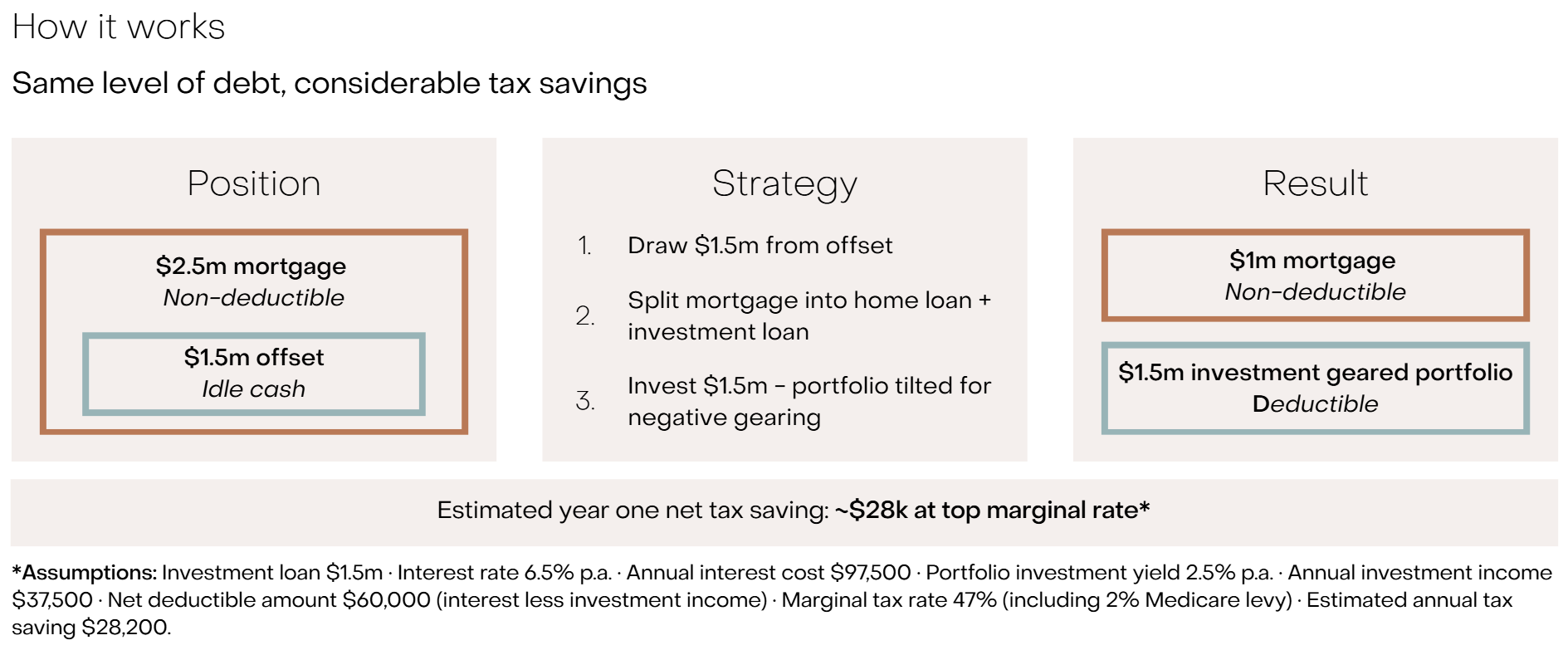

Consider Jess and Tim, a couple in their accumulating years with a $4 million home, a $2.5 million mortgage, and $700,000 combined in super. An early inheritance lifts their offset balance to $1.5 million. Rather than leaving this cash idle against the mortgage, they use it to pay down the mortgage and subsequently redraw the full balance of the offset account, using the cash to build a $1.5 million diversified portfolio. The interest on the $1.5 million is now tax deductible but more importantly, they have $1.5 million invested and growing for their future – that’s the key benefit.

The strategy suits clients with stable income, an existing mortgage with a redraw or offset facility, and a long investment horizon. It does not require a lump sum and can be built incrementally, with the deductible portion of the debt growing over time.

New investment property is now a cash flow proposition first and foremost. Without the annual tax offset for established property, the investment must justify itself on rental yield and capital growth alone. For many well-located properties, that case may still be sound, but the tax subsidy that previously lowered the holding cost is gone.

For clients drawn to negative gearing specifically for its income reduction benefit, shares and debt recycling now offer that same mechanism. The asset class has changed. The underlying tax logic has not.

With the CGT and negative gearing rules now settled, the opportunity lies in restructuring around them rather than waiting for further change. Clients weighing their next move, whether into shares, debt recycling, or property, should explore their options with their adviser to establish what fits their circumstances. Careful planning now can make a meaningful difference to long-term outcomes.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.