Financial Planning

In our recent research note ‘Private Credit in Context’, we reiterated our constructive view on the asset class amidst ongoing market volatility. Still, software sector concerns, rising default rates and redemption gates at prominent funds have led some investors to consider whether stress in private credit could trigger contagion that threatens the economic cycle. We seek to alleviate some of these concerns, drawing on recent analysis from the IMF, Federal Reserve and independent research.

Official assessments from the IMF and Federal Reserve stop short of calling private credit a systemic risk. While the sector has expanded to roughly US$2-3 trillion globally, this represents only 4-5% of global corporate lending, with bank credit to non-financial corporates exceeding US$50 trillion. Under a severe scenario where default rates reached Global Financial Crisis levels of 12%, total write-offs might amount to roughly 0.4% of US GDP, compared to 6-7% of GDP in estimated losses during 2008-09.

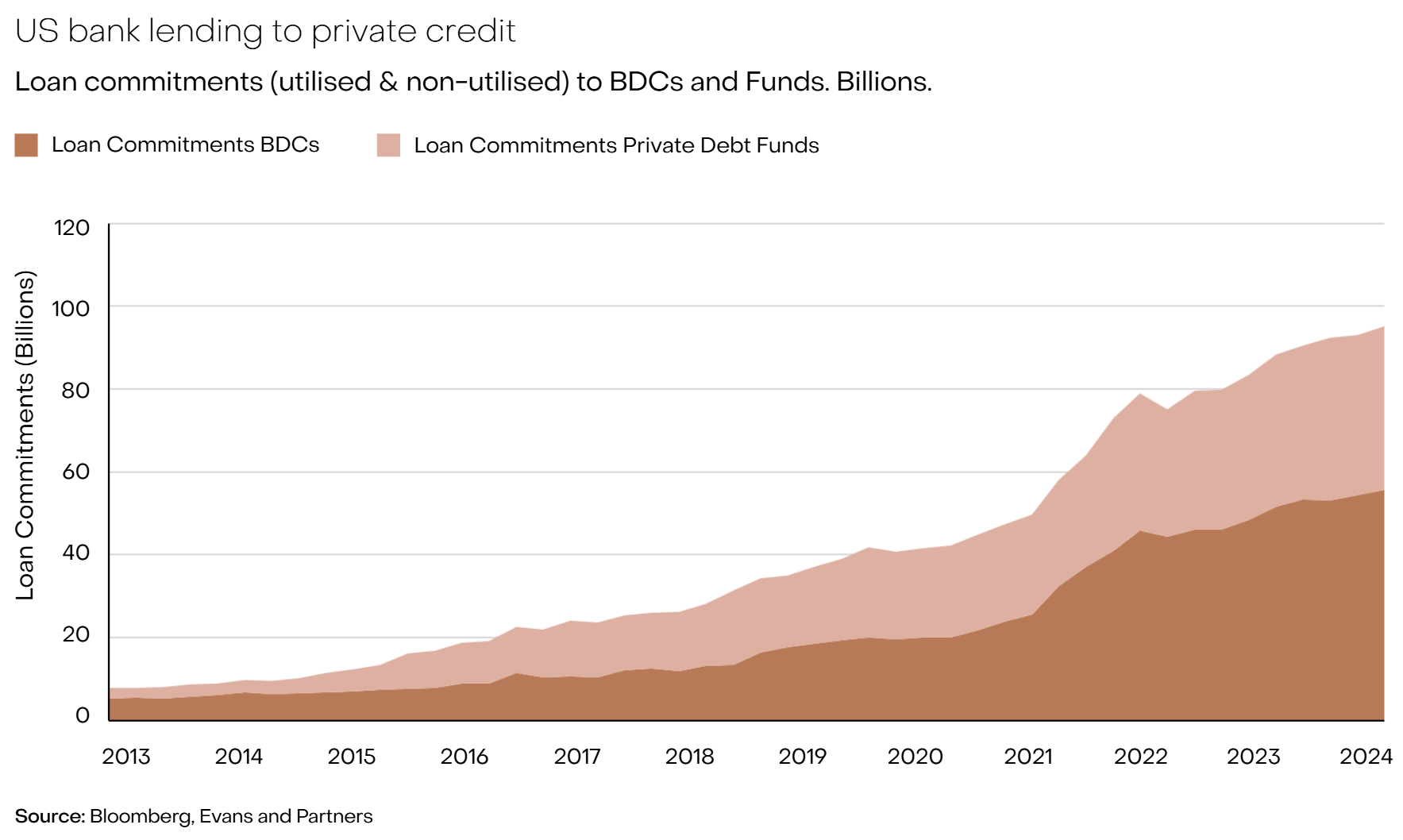

Banks do provide lending to private credit funds, estimated at roughly 5% of US bank loan portfolios, but these exposures are typically senior in the capital structure. Losses would first be absorbed by fund equity and junior investors before impacting bank balance sheets. The closed-end structure of most funds also limits run dynamics, as traditional closed-end funds require investors to commit capital for 7-10 years without redemption rights.

Perhaps most importantly, the investor base differs fundamentally from pre-crisis structured finance. Private credit losses would largely be borne by pension funds, insurers and other institutional investors rather than banks and households, substantially reducing the likelihood of widespread deleveraging cascades.

The more relevant consideration is indirect. Private credit has emerged as an important source of financing for mid-market companies, now accounting for a meaningful share of leveraged lending. If stress in private credit led to a pullback in new lending, it could tighten credit conditions for smaller firms that have limited alternative funding sources. This contrasts with the banking sector stress experienced during the Global Financial Crisis, where widespread deleveraging by major banks simultaneously restricted credit availability across the entire economy, amplifying the downturn.

The key difference is one of scale and interconnection. Banks are highly leveraged institutions whose capital constraints can force rapid deleveraging across their entire loan portfolios. Private credit funds, operating with far lower leverage and holding closed-end structures, face no comparable pressure to simultaneously reduce exposures across all borrowers. A more selective pullback in private credit lending would tighten conditions for affected borrowers but is unlikely to trigger the kind of systemic credit contraction seen in banking crises. Moreover, policymakers retain tools such as monetary easing and supervisory flexibility to address such dynamics if needed.

While recent headlines have raised contagion concerns, the evidence suggests these risks remain well contained. Private credit’s modest size relative to broader credit markets, structural protections limiting bank exposures, and closed-end fund structures all work to insulate the financial system. Official assessments from the IMF and Federal Reserve support this view.

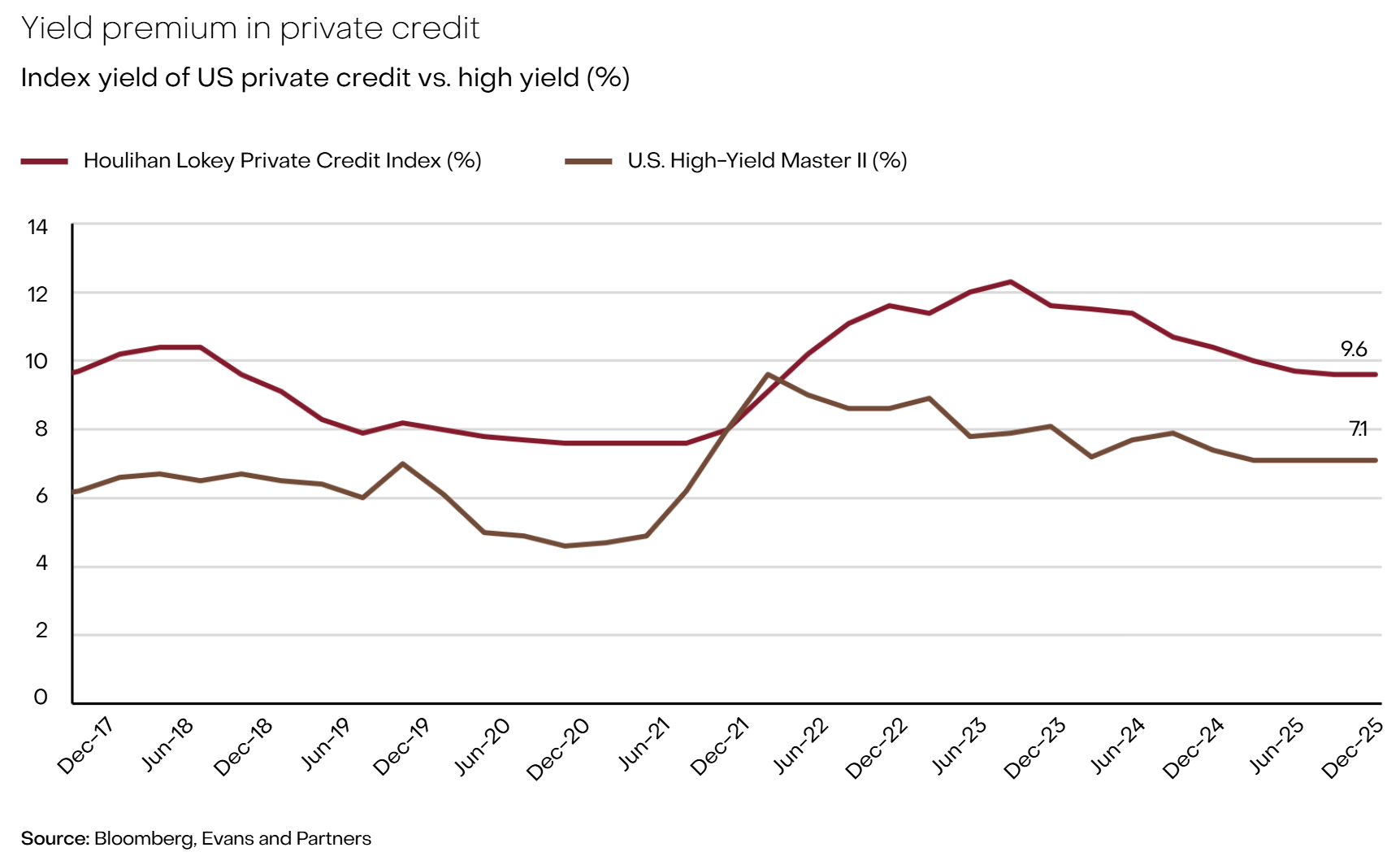

Critically, the market volatility has been driven more by investor anxiety about potential future developments than by actual credit deterioration. Default rates, while rising from historically low levels, remain well below crisis scenarios and substantially below what recent equity market sell-offs would imply. The disconnect between market pricing and fundamental credit performance suggests an overreaction to tail risks rather than a measured assessment of likely outcomes.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

This communication is not intended to be a research report (as defined in ASIC Regulatory Guides 79 and 264). Any express or implicit opinion or recommendation about a named or readily identifiable investment product is merely a restatement, summary or extract of another research report that has already been broadly distributed. You may obtain a copy of the original research report from your adviser.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.