Financial Planning

For much of the past two decades, investors benefited from genuine portfolio diversification. Low inflation, accommodative central banks, and stable global trade created a supportive backdrop where a balanced allocation across equities, bonds, and credit delivered consistent returns with manageable volatility. These assets moved largely independently, providing the natural portfolio balance that traditional frameworks relied upon.

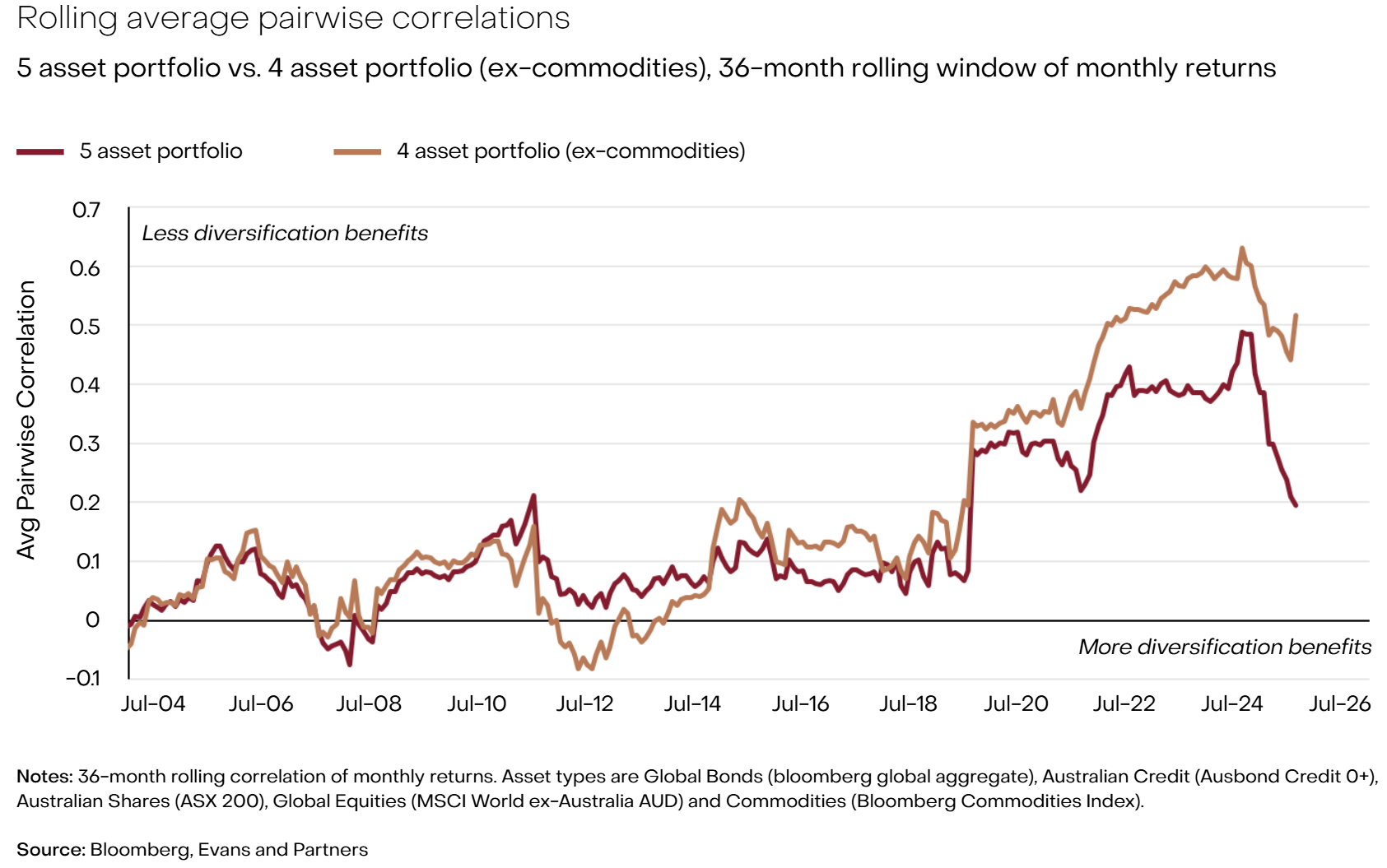

The data now tells a different story. A simple analysis of a 5-asset portfolio shows average pairwise correlations across a typical Australian balanced allocation (equities, bonds, credit, and commodities) hovered around 0.10 throughout the 2010s, indicating genuine diversification. Since 2022, that average has surged to 0.40-0.60, meaning assets are moving together rather than offsetting one another. That environment of low inflation and policy predictability has given way to persistent price pressures, constrained central banks, and supply-side disruptions. The chart is unambiguous: traditional diversification has broken down precisely when investors need it most.

The mechanism is straightforward. When inflation acts as a common shock, both equities and bonds decline simultaneously. Equities fall as higher discount rates compress valuations and margin pressures weigh on earnings. Bonds suffer duration losses as yields rise to compensate for inflation risk. The diversification assumption that underpinned decades of portfolio construction simply evaporates.

The Middle East conflict has reinforced these dynamics. Australian 10-year government bond yields have climbed to 5.0% even as economic data softens, with the RBA hiking into a supply shock while growth moderates. This is stagflation in practice: persistent inflation meeting weakening momentum. The likelihood of such scenarios has increased materially, and portfolios must adjust to this threat.

Our correlation analysis reveals a critical insight: portfolios including commodities experienced meaningfully lower average correlations (burgundy line) than traditional assets alone (brown line). During the 2022-2023 correlation spike, the 4-asset portfolio excluding commodities reached average correlations above 0.60 — meaning traditional assets were moving almost in lockstep.

The 5-asset portfolio including commodities peaked at 0.48, a material 12-percentage-point difference. This gap demonstrates that real assets offer genuinely differentiated return drivers, providing meaningful portfolio protection when traditional diversification failed most severely.

The chart demonstrates that commodities meaningfully reduced correlation risk, but expanding beyond this to include a broader alternatives allocation would amplify the benefit further. Infrastructure, with inflation-linked revenue streams through CPI escalators, showed even lower correlations to traditional markets during the 2022-2023 period. Asset-backed lending provides tangible collateral protection that insulates portfolios from operating business risk. Commodities, including (but not limited to) gold have historically delivered strong returns under stagflationary conditions.

Institutional investors maintain 20–40% allocations to alternative assets for precisely this reason. Private wealth portfolios averaging less than 10% in alternatives are structurally underweight the diversification tools the current environment demands. We are not calling for wholesale abandonment of equities and bonds — traditional assets remain central to long-term wealth creation. But portfolios must adapt.

We continue to build allocations to infrastructure, commodities, and asset-backed lending strategies as core diversifiers. These offer genuinely different return drivers that provide protection when traditional correlations break down.

This document was prepared by Evans and Partners Pty Ltd (ABN 85 125 338 785, AFSL 318075) (“Evans and Partners”). Evans and Partners is a wholly owned subsidiary of E&P Financial Group Limited (ABN 54 609 913 457) (E&P Financial Group) and related bodies corporate.

This communication is not intended to be a research report (as defined in ASIC Regulatory Guides 79 and 264). Any express or implicit opinion or recommendation about a named or readily identifiable investment product is merely a restatement, summary or extract of another research report that has already been broadly distributed. You may obtain a copy of the original research report from your adviser.

The information may contain general advice or is factual information and was prepared without taking into account your objectives, financial situation or needs. Before acting on any advice, you should consider whether the advice is appropriate to you. Seeking professional personal advice is always highly recommended. Where a particular financial product has been referred to, you should obtain a copy of the relevant product disclosure statement or other offer document before making any decision in relation to the financial product. Past performance is not a reliable indicator of future performance.

The information may contain statements, opinions, projections, forecasts and other material (forward looking statements), based on various assumptions. Those assumptions may or may not prove to be correct. Neither E&P Financial Group, its related entities, officers, employees, agents, advisers nor any other person make any representation as to the accuracy or likelihood of fulfilment of the forward looking statements or any of the assumptions upon which they are based. While the information provided is believed to be accurate E&P Financial Group takes no responsibility in reliance upon this information.

The Financial Services Guide of Evans and Partners contains important information about the services we offer, how we and our associates are paid, and any potential conflicts of interest that we may have. A copy of the Financial Services Guide can be found at www.eandp.com.au. Please let us know if you would like to receive a hard copy free of charge.

The information provided is correct at the time of writing or recording and is subject to change due to changes in legislation. The application and impact of laws can vary widely based on the specific facts involved. Given the changing nature of laws, rules and regulations, there may be delays, omissions or inaccuracies in information contained.

Any taxation information contained in this communication is a general statement and should only be used as a guide. It does not constitute taxation advice and before making any decisions, you should seek professional taxation advice on any taxation matters where applicable.

Fill out this expression of interest and you will be alerted when applications open later in the year.

Begin a conversation with an accountant who can help you with your self-managed super fund.

Begin a conversation with an adviser who will help you achieve your wealth goals.

Subscribe to get Insights and Ideas about trends shaping markets, industries and the economy delivered to your inbox.

Reach out and start a conversation with one of our experienced team.

Begin a conversation with one of our advisers who will help you achieve your wealth goals.

You can search for an adviser by location or name. Alternatively contact us and we will help you find an adviser to realise your goals.